Penalties for Wrong or Late XBRL Filing in Singapore

In the highly controlled corporate world of Singapore, proper and punctuality of financial reporting is not only a duty but also an expression of a companies governance and trustworthiness. Organizations had to file their financial statements using the eXtensible Business Reporting Language (XBRL) since it was implemented by the Accounting and Corporate Regulatory Authority (ACRA). XBRL framework also improves transparency, comparability and efficiency in the business ecosystem of Singapore.

There come with these advantages though stringent compliance requirements. Late or incorrect submissions may lead to serious punishment, damaged reputation and administrative inconveniences. To most firms and particularly SMEs, the complexities of XBRL filing are not correctly understood and thus preventable violations occur. This paper will deal with the implications of errors in filing or delay in filing, discuss the impact of wrong XBRL filing in ACRA and the fines and penalties to be incurred in XBRL filing in Singapore as well as provide an insight into how one can avoid making costly mistakes, especially for those involved in small and medium enterprise financial management training Singapore where compliance knowledge is essential.

1. Knowledge of XBRL Filing Role.

1.1 The XBRL Intention in Corporate Reporting.

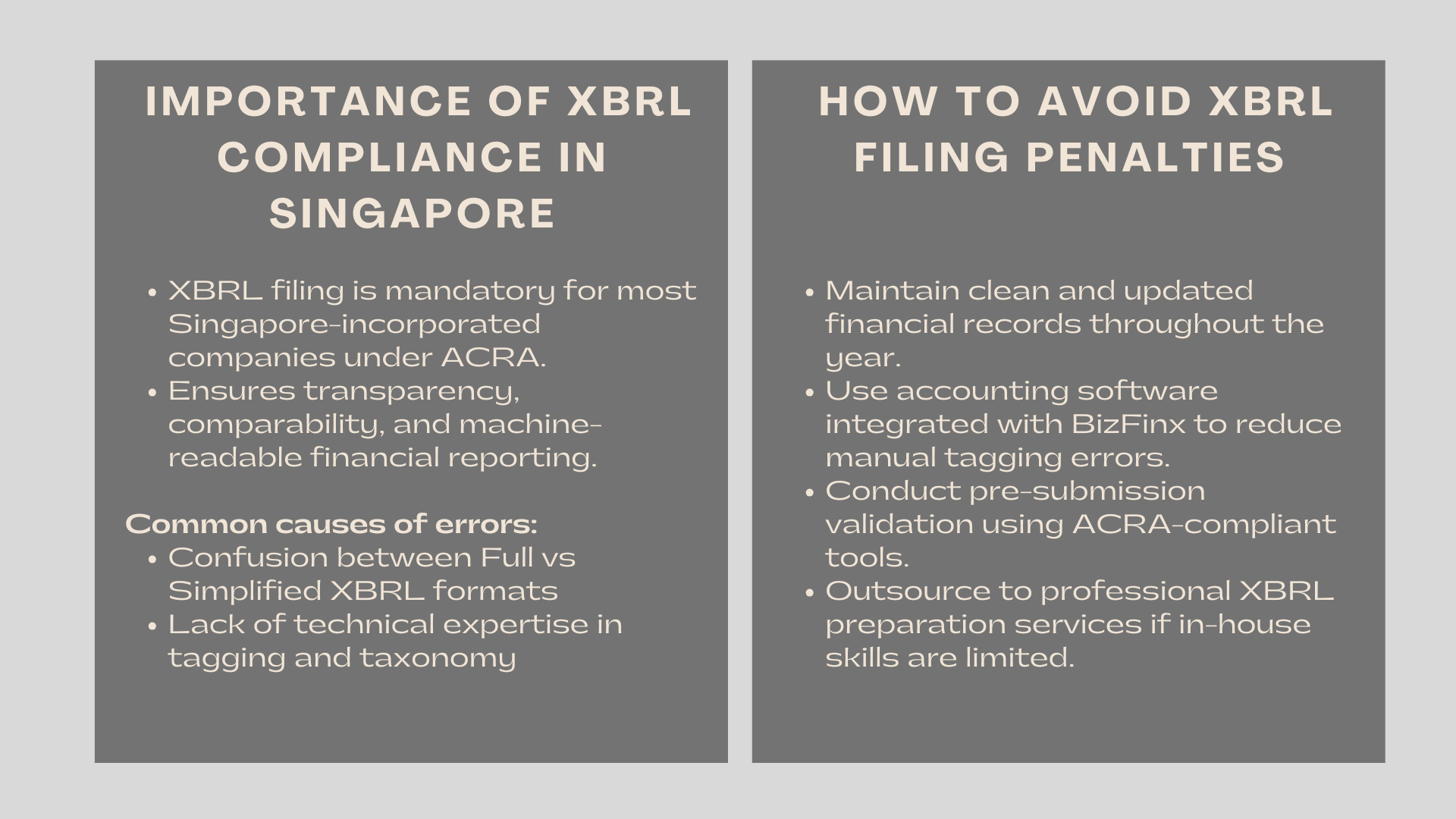

XBRL, which is often abbreviated as eXtensible Business Reporting Language, is an international standard that is utilized to transform a financial statement into a digital form in an effort to enable regulators, investors and analyst to work with large volumes of corporate data in an efficient manner. The ACRA in Singapore requires the majority of incorporated entities to present financial statements in XBRL format when they are submitting annual returns.

This standardization improves the accuracy and the accessibility of data. It enables the stakeholders to assess the performance and financial health of a company through uniform data that a machine can read. This shift to XBRL filing is in line with the overall initiative of Singapore to remain a transparent and pro-business financial center.

1.2 Companies that are impacted by XBRL Requirement.

All Singapore-incorporated companies, other than exempt private companies, foreign companies and limited liability partnerships, are obliged to be filed in XBRL. Depending on its size and complexity, entities should decide on whether to adopt Full XBRL or Simplified XBRL format.

An example is that smaller organisations that have simple financials can file a Simplified XBRL report, whereas large or publicly responsible organisations are obliged to file Full XBRL. Irrespective of the type, all companies are supposed to have some rigid deadlines and comply with the requirements of the taxonomy of ACRA.

2. Ordinary Reasons of Filing errors and delays.

2.1 Confusion of Filing Form.

Most companies cannot differentiate between Full and Simplified XBRL templates, and thus, they use tags incorrectly or do not fill out all the fields. The errors of misclassifying financial information, including the liabilities as a part of assets or the misreporting of equity may cause validation errors or rejection by the system of ACRA.

One instance is that, a middle-sized logistics company previously submitted a Full XBRL report when it should have submitted a Simplified XBRL, and this created discrepancies, which led to the late submission of its annual returns and financial fines.

2.2 Lack of Technical Expertise

Composing financial statements that comply with XBRL will not just need accounting skills especially technical skills such as familiarity with digital taxonomies and tagging software. Organizations that use manual data entry or untrained personnel frequently experience variation in the format, broken data connections or an absent component.

2.3 Poor Record Management

Proper XBRL filing is dependent on clean and modern accounting records. In situations where the financial statements are not reconciled properly all along the fiscal year, last minute filing usually results in hasty submissions and expensive errors.

2.4 Administrative Oversight

Deadlines to file are underestimated by many SMEs. The filing of annual returns is done in a period of seven months normally at the end of the financial year of the company. This is because a delay in scheduling internal reviews or board approvals may trickle down to late filings which leads to automatic fines.

3. The Impact of Making Filing mistakes.

3.1 Financial Fines and Penalties.

Among the shortest term consequences of non-compliance is a financial one. The fines charged by ACRA are progressive according to the duration the submission taken to be submitted. Those companies that fail to submit their filings earlier than a few days after the agreed deadline are automatically fined, which also gets higher with time.

In extreme cases, frequent submission delays may result in fines that are compounded and which, to a large extent, are a burden to the operations budgets. The fines and penalties for delayed XBRL submission in Singapore are designed to enforce discipline and encourage timely compliance.

3.2 Legal Implications and Director Accountability

According to the companies act, the directors of a company have a personal responsibility of ensuring that financial statements are filed correctly and on time. Non-cooperation can be persistent or willful, and the result can be prosecution and additional fines, or disqualification to serve more as a director in the future.

This accountability of the law strengthens the spirit of corporate integrity and financial transparency at Singapore. It highlights as well the significance of internal governance systems that have a focus on compliance.

3.3 Reputational and Operational Damage.

False or delayed filing represents a negative image of a company especially to investors and creditors who make decisions based on the financial statements. In addition, loan applications, mergers or licensing may be postponed due to rejected or invalidated filing.

As an example, one technology startup that wanted venture capital funding had its deal stalled because its XBRL submission of the previous year was rejected on two occasions due to data mismatch. These incidences show how failure to remain compliant may go beyond fines to deter growth prospects.

4. How to avoid Filing Errors: Best Practices.

4.1 Have Clean Financial Records Throughout the year.

Good accounting practices are the basis of mistake-free filing. Organisations are expected to keep up-to-date ledger books, balance accounts at the end of every month and all the changes are to be captured correctly in the financial statements.

4.2 Accuracy in Leverage Accounting Software.

Tagging and validation of data can be automated on modern accounting platforms to reduce the human error. Combining these systems with the BizFinx platform of ACRA, companies will be able to simplify submission and minimise the chances of technical problems.

As an example, cloud-based solutions, which can create XBRL-compatible files, may be used to test data with the taxonomy of ACRA before it is submitted, thereby allowing companies to identify errors at a very early stage.

4.3 Serve Professional Assistance.

In the case of firms with little in-house skills, firms that outsource XBRL preparation to accounting firms or corporate XBRL outsourcing can save on time and money. Experts know the peculiarities of the reporting taxonomy of ACRA and make sure that submissions follow all technical and legal requirements.

The price of outsourcing an external specialist might seem to be an added cost in the short term, but it will save the much higher cost of punishment, retasking, and even a tarnished reputation.

5. Strategic Investment in Compliance.

5.1 Improving the Confidence of Investors and Stakeholders.

On time and proper filing helps a company to improve its image of a well managed and reputable organization. Compliance is viewed by investors, lenders and prospective partners as a sign of good management and transparency.

5.2 Future Digitalization Preparation.

The business environment in Singapore is quickly going digital. Since ACRA is still developing its reporting infrastructure, those companies that implement effective filing systems now will be better placed in meeting the new requirements in future, which may include automated data-sharing or AI-based validation software.

The consequences of incorrect XBRL filing with ACRA serve as a reminder that compliance is not merely regulatory—it’s strategic. Companies incorporating reporting excellence in their practice have an upper hand of credibility and sustainability in the long run.

Case Study: Lessons Sisters can Teach on a Simple Violation of Compliance.

Take the case of a medium size construction company that failed to upload its 2023 XBRL report in time (45 days late). This delay was caused by the not fully complete tagging of information in the data and internal miscommunication between its finance and compliance departments. Late submission penalty was introduced by ACRA and directors of the company were warned in form of letters.

After the incident, the company introduced a disciplined compliance schedule, computerized its financial accounting and engaged an independent auditor to audit its financial statements after every quarter. The following fiscal year, it had full compliance, no punishments, regained its status with the ACRA and financial stakeholders.

This is to demonstrate that the challenge of compliance can be outcomes of proactive systems and timely coordination.

Conclusion to Penalties for Wrong or Late XBRL Filing in Singapore

The regulatory environment of Singapore does not provide any opportunity to commit any mistake in corporate reporting. XBRL filing is not a mere procedure requirement, it is a promise of accuracy, accountability, and transparency. Those companies that avoid such a duty will face financial and reputational consequences.

Being aware of the repercussions of filing the XBRL wrong with the ACRA and being aware of the fines and penalties of failing to file the XBRL with Singapore on time, businesses can protect themselves against an unwarranted risk. In addition to compliance, proper and timely reporting instills a certain level of trust, enhances good governance and prepares a business to take charge towards sustained growth within the competitive Singapore business environment.