Can LFMCs Manage Retail Funds?

Can LFMCs Manage Retail Funds? Understanding Their Role in Fund Management

The MAS oversees fund management in Singapore through the Securities and Futures Act. Fund Management Companies (FMCs) are regulated differently based on whom they serve and the kind of funds they handle.

It is very important to note whether a fund manager is directing funds for accredited/institutional clients or retail clients. Because of their increased risk and less sophisticated financial understanding, retail clients need more careful and regulated fund management.

In this article, we see if a licensed fund management company (LFMC) is able to invest retail investors’ money and examine the regulations and duties that they must follow. To better understand these obligations, professionals often turn to a compliance certification course for professionals to stay updated on MAS regulatory requirements and ethical standards.

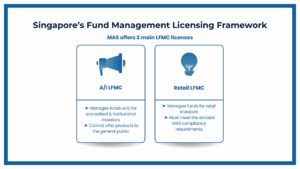

Singapore’s Fund Management Licensing Framework: Who Can Manage Which Fund?

MAS currently has three major licensing options for companies concerned with fund management.

1. Licensed Fund Management Company (LFMC) – Accredited/Institutional (A/I LFMC)

- Can care for investment funds exclusively for accredited and institutional individuals.

- Do not sell investment products to individuals.

2. Licensed Fund Management Company (LFMC) – Retail (Retail LFMC)

- Allows investment companies to take care of funds for retail investors.

- Companies in this area are required to meet the strictest regulatory and compliance laws from MAS.

To put it simply, a licensed firm that manages funds for retail investors must have a Retail LFMC license.

Who Are Retail Investors in Fund Management?

Retail investors are anyone who does not fall into the categories mentioned below.

- Accredited Investors (AIs) – these are people or organizations with a very high net worth.

- Institutional Investors (IIs) – generally consist of banks, insurers or sovereign wealth funds.

These investors often:

- Know little and have minimal experience with investing.

- Are in need of greater protection from financial products that might not suit them.

- There should be more transparency and stricter conduct protections.

As a result, MAS sets extra rules for managers of funds for retail investors to safeguard their interests.

Retail LFMCs: Additional Fund Management Requirements to Handle Retail Funds

Becoming a Retail LFMC involves meeting enhanced requirements in the following key areas:

1. Capital Requirements for Managing Retail Investor Funds

A minimum base capital of SGD 1 million is required for Retail LFMCs, exceeding the SGD 250,000 needed by RFMCs.

Apart from base capital, Retail LFMCs should keep some additional assets.

- Financial assets, in total, should be no less than 120% of their operational risk requirement.

- Additional funds are kept to cover both the repayment of redemption requests and everyday costs.

This support allows the FMC to carry on running and look after its investors, especially if the market goes down.

2. Compliance and Risk Controls in Retail Fund Management

Retail LFMCs ought to have tough internal controls and independent compliance functions set up such as:

- Someone in the organization (not managing the portfolio) who focuses solely on compliance.

- Clear policies described for covering risks due to investment, liquidity, credit and operations.

- You can have the audit work done by staff within your own business or by outside help.

- Accurate records must be kept and compliance breaches or exceptions must be constantly observed.

This way, the firm can handle its activities according to MAS rules and best industry standards. Businesses can also enhance internal oversight by adopting compliance and risk training solutions Singapore tailored to regulatory expectations.

3. Client Disclosure and Conduct Rules in Managing Retail Funds

MAS requires everyone in the industry to act responsibly towards retail clients.

- Procedures that help to identify a customer (KYC checks).

- Checking that a client’s risk level is appropriate for the selected product.

- Fees must be fair and all important information about fees needs to be included in product documents.

- Risk information should be prominently stated in prospectuses and offering memoranda.

Retail LFMCs are required by Fair Dealing Guidelines to be honest, transparent and focused on what is best for the customer.

4. Licensing Process to Become a Retail LFMC

A Retail LFMC license requires a detailed review from MAS. The application should be made up of:

- The organization has both a detailed business plan and a compliance manual.

- Information about important managers and their experiences.

- In addition to that, we must also prepare financial projections and capital adequacy statements.

- Any outsourcing that is in effect.

Usually, MAS interviews major officers in order to judge if they are fit and proper, have a proper understanding of risks and can comply with regulations.

It can take 4 to 6 months to complete the MAS application and the authority may ask for further details or straightaway reject those that don’t meet the rules.

5. Professional Indemnity Insurance (PII) for Retail Fund Managers

Most retail LFMCs (at times legally required) are advised to take out Professional Indemnity Insurance.

- Problems caused by negligent, incorrect or faulty actions in managing a fund.

- The operational risks are related to employee misbehavior or system-related problems.

As a result, retail investors are better protected from possible financial losses.

6. Annual Audit and MAS Regulatory Reporting for Retail Fund Managers

Retail LFMCs are expected to hand over their internal audited financial reports and news to the MAS, for instance.

- All financial statements for each year are prepared using Singapore Financial Reporting Standards.

- The first form is for capital adequacy returns.

- This form is used to show AUM and investments by quarter and also show you where your fees come from every quarter.

- Observed compliance statements from the CEO or Directors.

Late or wrong reports may end in penalties or the withdrawal of the license.

7. Fit and Proper Criteria for Retail Fund Management Personnel

Directors, CEOs, representatives and appointed representatives are all expected to meet MAS’ Fit and Proper Guidelines which analyze:

- Honesty, integrity and whether your reputation is good.

- Competency and capability in and of themselves.

- Financial soundness.

MAS asks Retail LFMCs to recruit fund managers who have handled money before within regulated markets.

Retail Fund Marketing and Distribution Rules Under MAS

Advertising and the way LFMCs are distributed must follow strict rules in retail to stop misleading or wrong selling.

All product advertisements, websites, brochures, and presentations must:

- Check the facts and don’t provide misleading information.

- Honestly tell users what they need to be careful about.

- If you advertise, do so according to the guidelines set by the MAS.

Under most circumstances, offering securities to consumers who intend to use them for retail purposes will require registration of the prospectus under the Securities and Futures Act.

Can an Existing A/I LFMC Serve Retail Investors?

It is not possible for an A/I LFMC to serve retail investors until the company receives Retail LFMC status. To do this, two types of traumas are needed:

- Meeting all the tougher rules and guidelines.

- Providing a new business plan and updated compliance system.

- The company going through more scrutiny and a separate approval by the MAS.

A/I LFMCs that accidentally promote their services or take funds from retail clients without licensing could experience major legal consequences.

- License revocation.

- Fines and penalties are a part of tax law.

- Threat of or actual public criticism or penalties.

Benefits and Responsibilities of Managing Retail Investor Funds

Helping retail investors with their money allows you to access more markets.

- More investors can be involved.

- More people know the brand.

- Expected growth in assets managed.

Yet, achieving these benefits means complying with many more demanding requirements.

- More money spent on running the organization.

- Within the financial services industry, companies are expected to report more often to regulators.

- More opportunities for being sued or inspected by authorities.

Before participating in the retail sector, FMCs have to carefully match their commercial advantages with their rules and costs.

Conclusion

Conclusion

Those looking to manage funds for retail customers need to first obtain a Retail LFMC license. The rules for capital, compliance, disclosure and client protection in this license are much stricter than with other licensing.

Key Takeaways:

- Only Retail LFMCs are empowered to take charge of retail investors’ money.

- LFMCs engaging in retail activities must stick to stronger capital, risk management and operational standards.

- A/I LFMCs or RFMCs cannot accept any business from retail clients by law.

- To get a Retail LFMC license, you must go through a long and specific process with MAS.

- Managers of retail investor funds must meet higher demand for oversight and have more obligations under regulations.

Before entering the retail investment market, a fund management company must be ready with thorough planning and effective guidance by experts to comply with MAS terms.