Guide to Singapore’s Goods and Services Tax (GST) Registration

Introduction to Guide to Singapore Goods and Services Tax

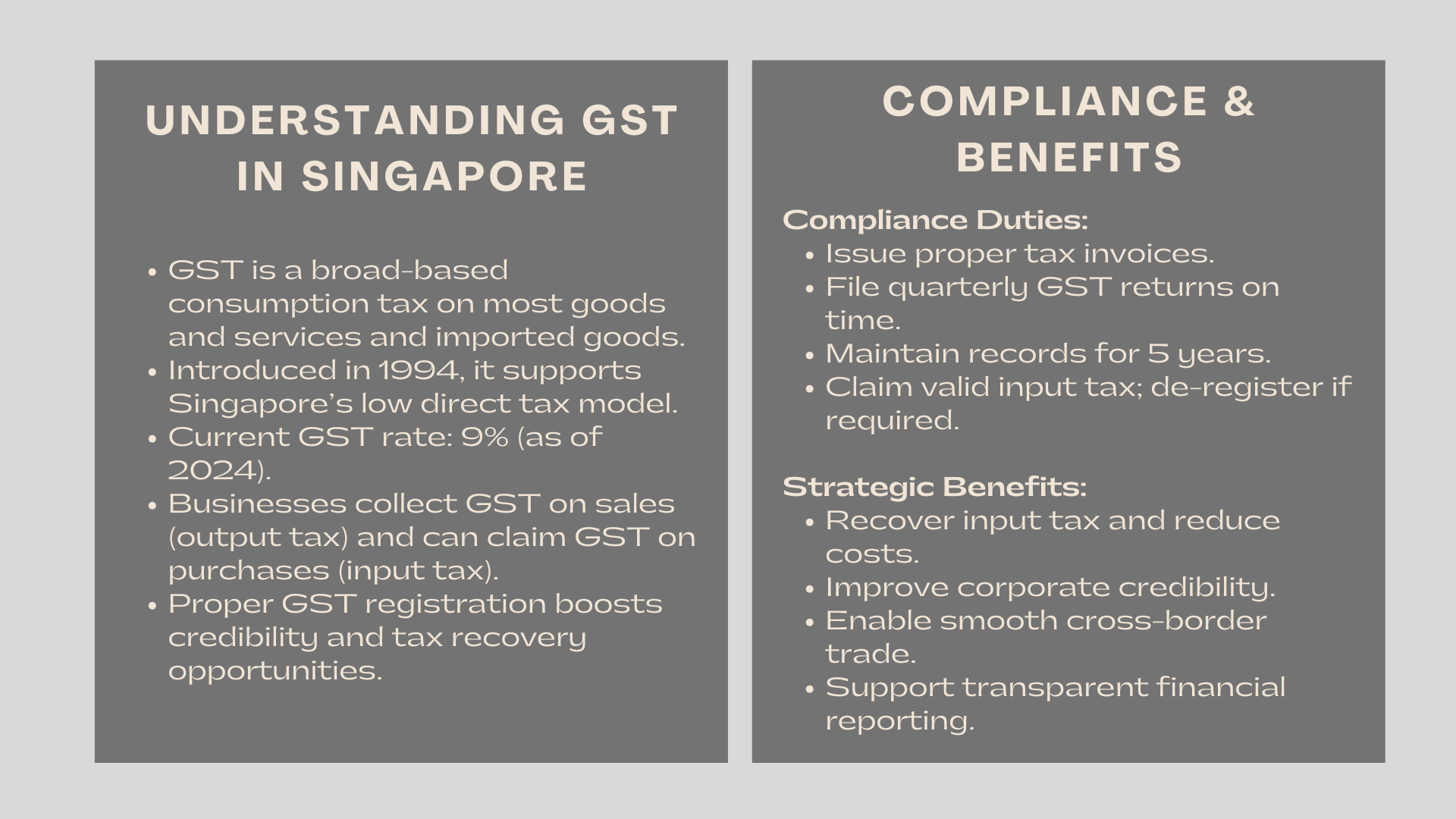

Singapore has a taxation regime that is widely recognized to be simple and the business-friendly environment, which was meant to ensure compliance through local and foreign firms. The Goods and Services Tax (GST) is one of the most significant elements in this system and which is a consumption tax, which is broad based and is imposed on most goods and services provided in Singapore and also on imported goods.

Since its introduction in 1994, GST has been one of the major sources of revenue to the government as well as ensuring that Singapore has low direct tax rates. Familiarity with the time and the mechanism of GST registration is crucial to all businesses within the country, including those seeking tailored compliance solutions for asset management firms. A failure to respect registration requirements may in turn attract penalties and lost prospects of recovering taxes.

The meaning of GST and the significance of GST.

The GST of Singapore is operated in much the same way as Value Added Tax (VAT) in most of the other countries. It makes sure that each business gathers and pays tax on the value that they add to goods or services at every production or distribution stage of production.

The normal GST rate is now 9% (as of 2024) on a majority of the taxable supplies. Companies collect GST on their sales (output tax) and are allowed to obtain credits to the GST they paid on business purchase (input tax). The disparity between the two is paid or refunded to the Inland Revenue Authority of Singapore (IRAS).

The registration of GST has multiple functions: it legitimizes tax liabilities of a business, it increases business credibility among the clients, and it allows the businesses that are eligible to get back a part of the input taxes on purchases and expenses.

Who Needs to Register for GST?

Depending on the income and operations of their businesses, business in Singapore would have to decide whether their registration is mandatory or optional.

Compulsory Registration

A business should be registered to pay GST in either of the following conditions:

- Retrospective Basis: In case your taxable turnover has been more than SGD 1 million within the last 12 months.

- Prospective Basis: In case you are reasonably expected to turn over more than SGD 1 million within the next 12 months in terms of taxable income, i.e. because signed contracts or projected sales.

Any failure to register when necessary may result in penalties, fines and retroactive GST payable, including tax on previous sales.

Voluntary Registration

Although the turnover of a company might be less than the SGD 1 million limit, a company can still apply to become a voluntary GST-registered company. Startups, exporters, or businesses whose main suppliers are registered by GST make this option, and in this case, they can claim input tax credits.

Nonetheless, voluntarily registered companies have to remain registered at least two years and keep proper recordkeeping and compliance during such time.

Step-by-Step Guide to GST Registration

To simplify compliance, IRAS has made the GST registration process efficient and largely digital. Below is a step-by-step guide to GST registration process for Singapore companies that outlines what every business should know before filing.

Step 1: Determine Eligibility

Make sure that your business is compulsory registered or optional before making an application. This is by computing your total turnover that is taxable which includes local sales, services and exports of goods.

Step 2: Take the e-Learning Course (in case of the Voluntary Applicants)

In case, your company has filed GST registration voluntarily, IRAS would insist that you take an e-Learning course named Overview of GST. This will make sure that the applicants are aware of their liability to the GST Act.

Some companies, including those operated by the Accredited Tax Advisors or GST Consultants might be exempted of this point.

Step 3: Make the necessary documentation.

You will be required to compile and file required documentation which include:

- ACRA registration details of business.

- Financial statement or management account copies.

- Expected sales or signed contracts to your favor.

- Evidence of business transactions (e.g. invoices, contracts or bank statements)

Step 4: Make the GST Registration Application.

Applications are made electronically on the myTax Portal on the IRAS website. The businesses need to make sure that all the details are correct, in order to delay the processing.

When lodged, IRAS normally requires 10 working days to process compulsory registration applications and a little more in voluntary ones.

Step 5: Waiting to get your GST registration number.

Upon the approval, your company will be given a GST registration number and an effective date of registration. And henceforth you need to start levying GST on taxable supplies and start putting your GST number on all invoices.

Requirements and Procedures for GST Compliance

After registration, companies must adhere to the requirements and procedures for registering a business for GST with IRAS in Singapore, which include proper recordkeeping, filing returns, and timely tax payments.

Issuing Tax Invoices

Taxable sales that are more than SGD 1,000 must attract a tax invoice by all GST-registered companies. Such invoices should have the GST registration number, date, goods or services description, and the GST charged clearly displayed.

Filing GST Returns

Registered businesses are required to submit GST returns in quarterly submissions in the myTax Portal. The return is a summation of the sales, purchases, output tax and input tax.

The payments or refunds of GST should be made within a month of the accounting period. Penalties can be fined on late filings or payments.

Maintaining Proper Records

The transactions must be recorded in details by the businesses to a minimum of five years. These are tax invoices, receipts, contracts, import / export documents and accounting ledgers. Good documentation is a guarantee of compliance in the IRAS audits.

Claiming Input Tax

Input tax credit can be claimed by companies on GST paid in regard to business related expenses in the office rent, utilities, raw materials and equipment. Claims however are not admissible on items such as entertainment or personal purchases.

De-Registration

The company can seek GST de-registration in the event that it stops its operations or its taxable turnover is below SGD 1 million and it is not expected to experience growth in its turnover. IRAS should be informed 30 days after stopping to escape punishment.

Benefits of GST Registration

Although GST registration promises to increase administrative burdens, it is also associated with some benefits in terms of strategy:

- Input Tax Recovery: The business will be able to recover GST charged on purchasing inputs and save on the total operating expenses.

- Better Credibility: GST-registered businesses tend to look more professional to the clients, particularly bigger companies and government

- The Support of Cross-Border Trade: The exporters enjoy zero-rated GST on international sales yet they can claim the input taxes.

- Transparency and Compliance: GST registration enhances good corporate governance and generates an improved financial reporting

These benefits ensure that GST registration is not only a legal necessity but it is also a wise business move towards sustainable viability.

There are also some errors that should be avoided when registering GST.

Although the process is very simple, there are several mistakes that companies commit in the application or maintenance of the GST registration. The following are some of the typical errors:

- Error in Turnover Calculation: There are several taxable income streams that are not processed when determining eligibility.

- Late Registration: Not time bound registration could result in late GST

- False Filings: Misunderstanding of input or output taxes may become a trigger to commentaries or audits.

- Other Reasons that may cause rejection of tax claims or fines include failure to keep records.

These pitfalls should be avoided so as to have a smooth registration and make it compliant with the IRAS.

Professional Advisor Support.

Going through the GST rules may be not that easy and it may be difficult to follow for foreign investors or even startups with no background on the tax environment in Singapore. The process can be made easy by outsourcing the services of qualified tax advisors or accounting firms to avoid compliance risks.

These specialists may help in:

- Determining the eligibility and the time of registration of GST.

- Developing and completing documentation.

- Quarterly management of GST filings.

- Processing audit or mail with IRAS.

Collaboration with professionals will make sure that businesses are in good terms with local taxation bodies as well as will optimize their performance.

Conclusion

The GST registration is a very important step in every business located in Singapore. Not only does it satisfy a legal requirement but also it is also an indicator of financial transparency and financial credibility in the market. Companies are able to provide an effortless compliance and sustainable growth by familiarizing themselves with the rules of eligibility, ensuring that they properly keep the records and adhering to the filing procedures.

To both the entrepreneurs and the foreign investors, the understanding of GST regulations early in the incorporation process forms a basis of effective tax management and success in the business in the long run in Singapore.