What Are the Restrictions on the Types of Funds a Venture Capital Fund Manager (VCFM) Can Manage?

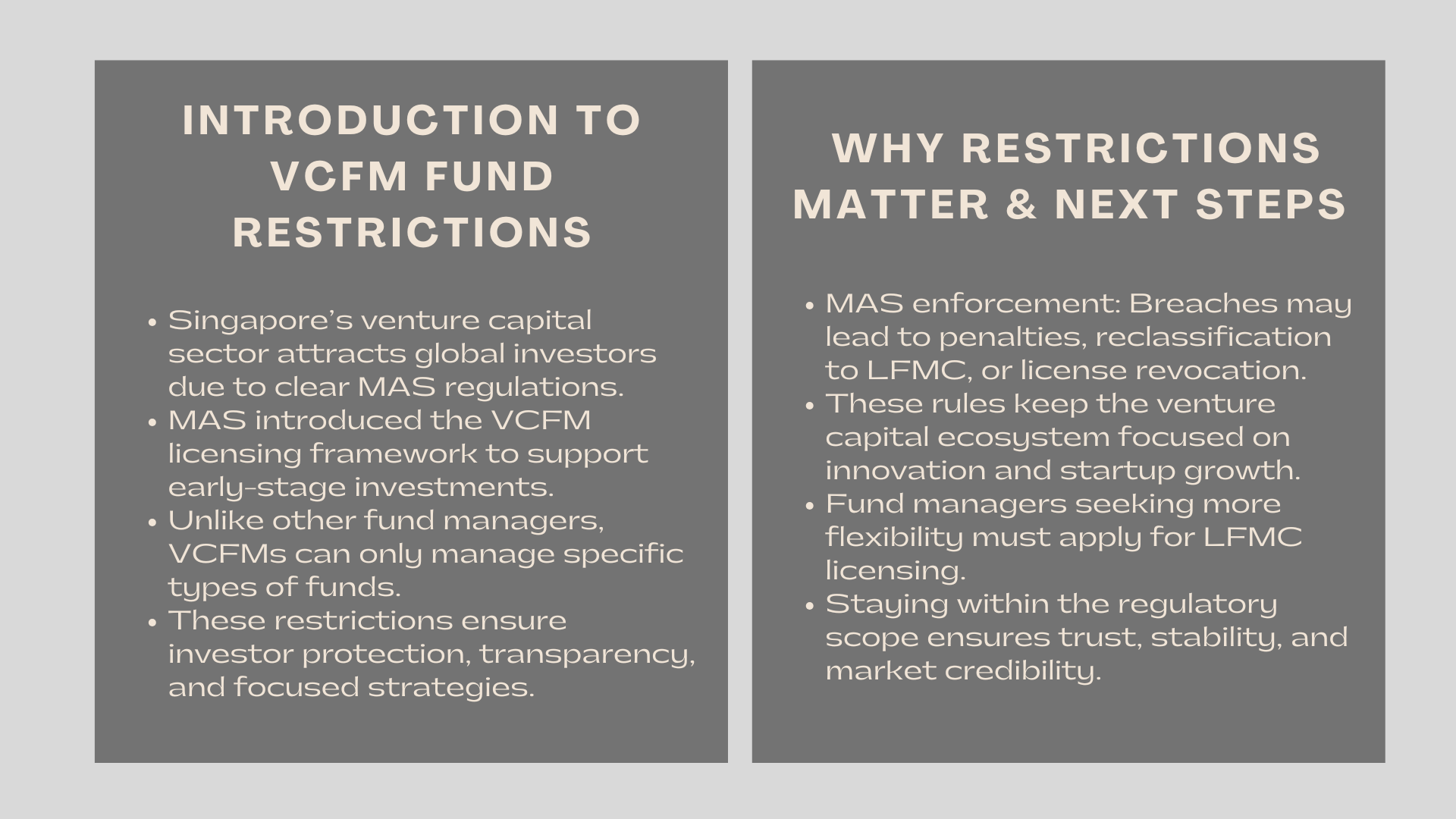

The country is a major recipient of venture capital in Asia due to reliable regulations and a flourishing community of entrepreneurs. MAS launched a simplified regulation for managers of Venture Capital Funds (VCFMs) to encourage early-stage investment and attract global investors through the Venture Capital Fund Manager licensing framework in Singapore.

Instead of having many regulations, the VCFM license does not allow a firm to manage all types of funds. The rules are put in place to keep venture investing trustworthy, looking after clever investors and clarifying matters for regulators.

This article looks closely at the funds a VCFM can deal with and the limits set by the MAS for licensing.

1. Overview of the VCFM Regulatory Framework

1.1 What is a Venture Capital Fund Manager?

A Venture Capital Fund Manager (VCFM) is an organization that has been approved by MAS to deal with funds majorly investing in private, start-up businesses. Often, the venture capital firm invests in new companies in industries such as technology, life sciences, fintech, sustainability and others that are expected to grow rapidly. The MAS VCFM regulatory compliance requirements ensure transparency, investor protection, and adherence to best practices in Singapore’s asset management sector.

The Venture Capital Funds Management Licensing Framework (VCFM) began in 2017 to facilitate the regulatory process and increase interest from capital managers in Singapore.

1.2 Why Are There Restrictions?

Because they are regulated differently, VCFMs do not have to hold capital, operate audits on their risks or fulfill many other compliance standards. However, to maintain the focus of VCFMs on venture capital, MAS sets strict rules on fund strategies and structures, ensuring that VCFM licensing requirements for managing venture capital funds in Singapore remain clear and investor-focused.

2. General Restrictions on VCFM Fund Management Activities

It states clearly in its guidelines which funds VCFMs can be responsible for. Following are the main restrictions:

2.1 Funds Must Be Venture Capital in Nature

A VCFM has the authority to look after only those funds that meet the definition of venture capital. According to MAS, these funds have various requirements.

- Before anything else, focus on buying shares of startup or early-stage businesses that are still unlisted.

- Identify companies that are growing at a rapid rate.

- Avoid trying to earn quick profits through risky strategies.

- Consider your investment needs for a long span of time.

Consequently, this approach supports the main role of venture capital which is to give patient time and money to enterprises offering the potential for high-risks and high-rewards.

2.2 Closed-End Fund Structure

VCFMs have to handle closed-end funds that feature the following characteristics:

- The money invested cannot be withdrawn by the investor whenever they like.

- Money is held with the project for a fixed time, generally between 7 and 10 years

- There are only a few dates each year that allow people to subscribe to the fund.

This type of investment allows fund managers to invest steadily into startups since they do not have to worry about cash being taken out on a regular basis.

2.3 Target Investors Must Be Accredited or Institutional

Retail investors cannot have their money managed by a VC firm. They are only allowed to obtain and manage funds from:

- High-income or high-asset people and companies are called accredited investors (AIs).

- Institutional investors include financial institutions, government groups and big companies.

Since investing in venture capital is more challenging and risky, only investors with advanced knowledge are allowed to participate.

3. Types of Funds a VCFM Cannot Manage

3.1 Hedge Funds and Trading Strategies

Dealing with hedge fund management or utilizing strategies that involve hedge funds is forbidden for VCFMs.

- Short selling

- High-frequency trading

- Derivatives are used by investors for speculating purposes.

- Traders use market timing or arbitrage to find profitable opportunities.

Those strategies are different from venture investment and are subject to a different set of rules. If you are a manager and want to use these strategies, you must first get an LFMC license.

3.2 Funds with Redemption Rights

Any fund where people can redeem their units or shares any time is not allowed under the VCFM regulations. These types of investments are classed as open-end funds.

- Mutual funds

- Unit trusts

- Liquidity funds

VCFMs need to make sure that before the fund is invested, investors do not have a way to get their investment back before the maturity date.

3.3 Leveraged or Derivative-Based Funds

According to MAS, VCFMs are not allowed to control funds used for payments.

- Leverage allows you to benefit from higher returns.

- Use the practice of margin trading.

- Devote a large portion of your investments to derivatives and special products.

Leverage causes funds to face risks that are difficult to manage for long-term ventures.

3.4 Real Estate or Infrastructure Funds

Certain investments go past the spectrum of what a VC fund manager can handle.

- Real estate is made up of assets.

- Infrastructure projects

- You can invest through REITs or companies focused on developing property.

The regulations for these funds are different since their assets are large, they take a long time to repay and their value calculations are not always simple.

3.5 Funds Focused on Public Equities

Trading in listed securities or publicly traded shares is not considered venture capital, so it is not permitted there. Simply targeting small companies or rising markets is not enough; to be considered venture capital, the fund ought to focus only on investing in private and early-stage firms.

4. Characteristics of Permissible Funds Under the VCFM Regime

Always, the funds an asset manager manages must comply with certain criteria.

- Investment Target: Unlisted, early-stage businesses (typically startups)

- Fund Structure: Closed-end, fixed-term

- Investor Type: Accredited investors and institutional clients only

- Exit Strategy: IPO, acquisition, or secondary sale after long-term holding

- Return Profile: High-risk, long-horizon returns with capital gains at exit

- No Redemption Rights: Investors cannot redeem funds before term maturity

- No Leverage or Derivatives: Fund cannot use borrowed capital or speculative instruments

5. Implications of Breaching Fund Restrictions

5.1 Regulatory Penalties

If VCFM manages funds outside what is allowed, MAS could:

- End or postpone the fund manager’s ability to manage investments

- Ensure there are penalties in place for offenders

- Exclude the directors or CEO from submitting new applications in the future

5.2 Reclassification as LFMC

If a fund manager does not follow the limitations on allowable funds set by MAS, the regulator may consider the firm to need a full CMS license, with more strict requirements and rules to follow.

5.3 Legal and Investor Risks

Fund managers can face challenges, should they work beyond the VCFM framework.

- Investors can bring civil lawsuits against a company.

- When fiduciary duty is not met, charges can be made.

- The redemption or the process of retrieving money from investors

As a result, it is necessary to only engage in activities approved by MAS for VCFMs.

6. Transitioning from VCFM to LFMC

Various funds start by being VCFMs, yet at some point they can want to change their investment strategies or attract other investors. As such, they have to apply for a license to manage money under the CMS, choosing from the A/I or retail LFMC categories.

Fnd managers become able to:

- Offer the opportunity to retail investors (for Retail LFMCs)

- Provide flexible opportunities for fund setting

- Look beyond stocks and invest in items such as real estate and hedge funds.

Nevertheless, the firm will need to comply with tougher requirements, raise more capital and be supervised more often by the MAS.

7. Conclusion to What Are the Restrictions on the Types of Funds

While the VCFM in Singapore allows early-stage startup fund managers to register in a simple way, there are clear boundaries to this option. VCFMs must:

- Manage funds that are closed-end only.

- Mainly invest in private companies that are in their early years.

- Do not work with retail investors, focus on avoiding hedge fund strategies, skip real estate and do not engage with public equities.

As long as these restrictions are followed, startups and venture capitalists remain subject to regulations and support the purpose of encouraging innovation. Managers aiming to invest in more types of financial assets should get new licenses that allow them to do so.

It is vital for both regulations and building trust that a VCFM knows which funds it can manage successfully in Singapore’s asset management market.