MAS Compliance Readiness Gap Analysis

Singapore has one of the most stringent regulatory frameworks in the Asia-Pacific region that governs the financial services landscape in Singapore. The heart of this structure is the Monetary Authority of Singapore (MAS), which not only plays the role of the central bank of the country but also acts as the integrated financial regulator of the country. To the financial institutions that conduct business in this jurisdiction, compliance is not a matter of periodically doing so, but rather it is an institutional matter that should be done at all times. However, it is common in many organizations, especially where there is rapid expansion or where a restructuring of the organization is being undertaken, that compliance gaps: misalignments between the current operational state of the organization and the standards set by the regulator are accumulated.

A regulatory gap analysis of Singapore-based firms is fundamentally an organized diagnosis procedure. It helps institutions to recognize areas where their policies, procedures, systems, and culture are below what is expected by the regulatory bodies. In contrast to a regular audit, in which the main emphasis is on historical accuracy, a gap analysis is a proactive one. It poses the question: Were MAS to investigate our operations today, what would they discover? This framing renders it an important tool not just to the established banks and licensed fund managers but also to the growing mid-sized institutions whose compliance infrastructure has not kept pace with business expansion.

This paper is a practical review of the gap analysis process as it relates to the MAS-regulated entities. It takes a tour of the major stages of the assessment process, the pitfalls that can arise, and the lessons that have been learned by some experienced compliance professionals in their experience of the assessment process. Whether you are a compliance analyst coming into your first major review, a risk manager supporting a licensing application, or an operations professional, who is seeking to understand what regulators look at or why they are important, this guide will provide you with a concrete, structured understanding of how readiness assessments are undertaken and why they matter.

Understanding the MAS Regulatory Landscape

MAS has supervisory authority over banking, insurance, capital markets, and payment services, where each sector is regulated by specific legislation and subsidiary notices. The regulatory perimeter is defined by the Banking Act and the Securities and Futures Act and the Financial Advisers Act and the Payment Services Act. To the compliance professionals, the first step in a gap assessment is to understand what Acts and MAS Notices apply to the activities of their institution. Such a lack of understanding of the extent of rules to be applied is in itself a compliance gap – and a surprisingly frequent one at that.

The MAS licensing compliance requirements are set out in detail and depend on the type of license. A capital markets services license holder, such as a major payment institution, has various obligations as compared to a major payment institution. These requirements extend beyond the conditions that accompany the license itself, such as capital adequacy, fit-and-proper criteria of key personnel, and business conduct requirements, but also cross-cutting requirements that relate to anti-money laundering (AML), counter-terrorism financing (CFT), technology risk management, and business continuity planning. The scope of these requirements implies that compliance staff have to work hand in hand with legal, finance, operations and technology colleagues in order to conduct a truly comprehensive gap review.

Another factor that should be understood is that MAS is an active regulator. It publishes thematic inspection findings and publishes industry guidance notes and updates its regulatory framework in response to international standards in bodies such as the Financial Action Task Force (FATF) and the Basel Committee on Banking Supervision. Gap analysis is not a one-time thing. Treating it as they do, institutions are often left behind as the regulatory goal posts are moved. In the best practice, it is a structured annual review complemented with triggered assessment whenever MAS publishes new guidelines or when there is a material change in the business model of the institution.

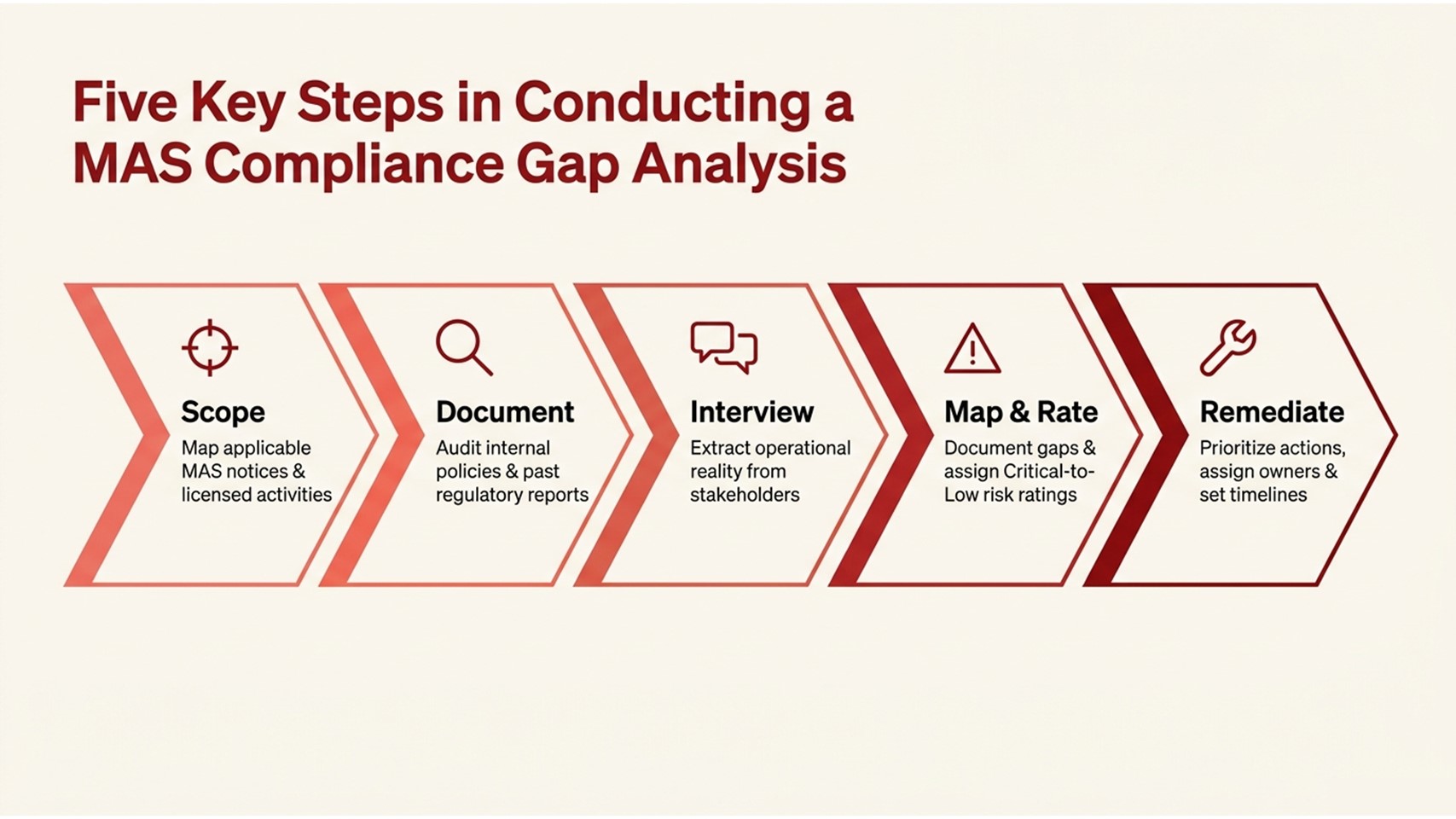

Five Key Steps in Conducting a MAS Compliance Gap Analysis

A properly designed gap analysis is based on a rigorous approach. The five steps that follow are the essence of the process as implemented by the best compliance advisory teams in Singapore and abroad.

Step 1 — Define the Scope and Regulatory Inventory: The initial step involves mapping the entire MAS notice, Act provision, and guideline applicable to the institution. This regulatory inventory will be the foundation on which the existing practices will be assessed. The scope definition must be based on the type of license that the institution has, its business operations, and its customer groups.

Step 2 — Collect and Review Internal Documentation: The team reviews policies, procedures, board minutes, past MAS examination reports, audit findings, and incident logs. This documentation analysis shows that there are formal gaps in written policies as well as indicators of control failures and deficiencies in enforcement.

Step 3 — Conduct Stakeholder Interviews: Structured interviews with the compliance, legal, finance, technology, and business heads present the reality of operations behind the documents. Frequently, written policies are present on paper only, but are not put into practice; thus, interviews are a more reliable means of discovering the implementation gaps in practice than a review of the documents.

Step 4 — Map Gaps and Assign Risk Ratings: Each identified gap is recorded in a gap register and given a risk rating – usually Critical, High, Medium, or Low – based on the probability of regulatory action and the potential impact of the action on the license, customers, or financial position of the institution.

Step 5 — Develop and Prioritize the Remediation Plan: The last step will convert the gap register into a plan of action. Owners of each gap are identified, a specific date when the gap will be remedied, and quantifiable success criteria. The plan is offered to the board or a board-level committee to be signed off on and monitored.

The table below illustrates common compliance gap areas identified during MAS reviews:

| Compliance Area | Typical Gap Found | Risk Level |

| AML/CFT Controls | Partial customer risk profiling. | High |

| Technology Risk | Largely old-fashioned IT security policies. | Medium–High |

| Financial Reporting | The lack of alignment with the standards of the IFRS. | High |

| Licensing Conditions | Scope creep beyond licensed activity | Critical |

| Board Governance | Lack of strong audit committee supervision. | Medium |

Table 1: Common MAS Compliance Gap Areas and Risk Levels

The process flow below illustrates how these five steps operate in sequence:

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Step 6 |

| Scope Definition | Documentation Review | Stakeholder Interviews | Gap Mapping | Risk Prioritisation | Remediation Planning |

| Determine licensed activities & MAS notices that may be used. | Audit procedures, policies and historical correspondence of the MAS. | Legal, Interview compliance, finance and op teams. | Compare the current state vs MAS requirements. | Put gaps in the categories of their severity: Critical / High / Medium. | Allocate owners, timeframes and measurement of tracking. |

Process Flow 1: MAS Compliance Gap Analysis — Six-Stage Assessment Workflow

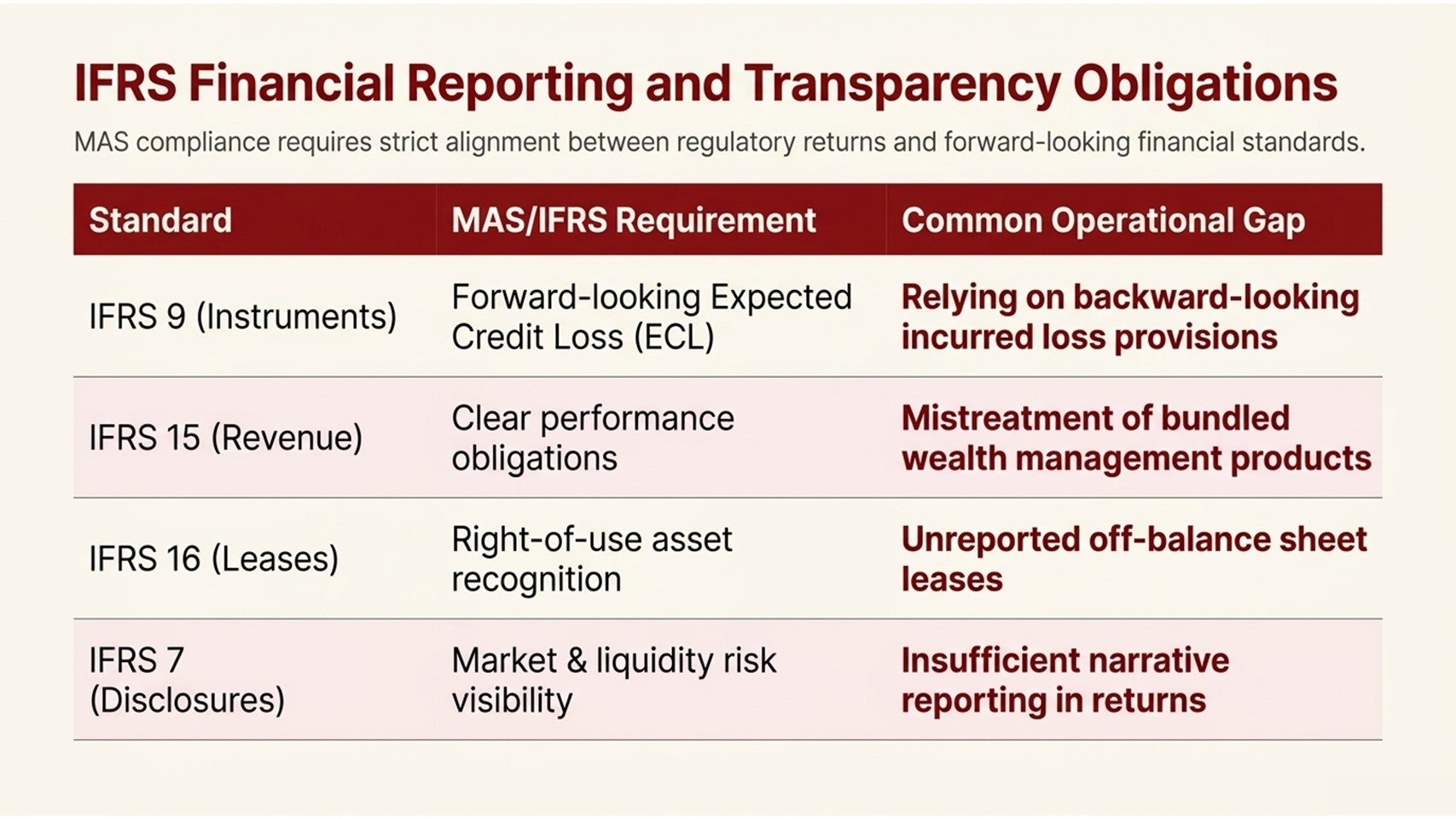

IFRS Financial Reporting and Transparency Obligations

One of the aspects of MAS compliance that has often been overlooked by non-finance professionals is the overlap between regulatory compliance and financial reporting. Entities that fall under the control of MAS must prepare and submit financial statements and regulatory returns that are prepared in accordance with the prescribed standards. To most institutions, this implies compliance with the IFRS financial reporting transparency requirements, such as the application of applicable International Financial Reporting Standards in their balance sheet, income recognition practices and disclosure obligations.

With the introduction of the IFRS 9 (replacing IAS 39), there was a major change in the way credit losses in financial institutions are recognized and measured. Under the new IFRS 9, the institution will have to adopt a forward-looking Expected Credit Loss (ECL) model instead of the older incurred-loss approach. The methodology needed to develop strong ECL models remains a challenge to many smaller institutions and new licensees in Singapore, especially in cases where the history of the events to be modeled is not long. This gives a reportable gap in both IFRS financial reporting transparency and MAS regulatory returns since the ECL calculation feeds directly to capital adequacy computations.

In addition to IFRS 9, institutions also need to address IFRS 15 on revenue recognition, which is particularly relevant to wealth management institutions, with complex fee structures and many branches. As part of a gap analysis, the financial reporting review aspect usually encompasses the Finance and accounting team and compliance team to ensure that the institution’s reporting practices are within the requirements of IFRS as well as the MAS return templates, which are specific to each institution. Any lack in this regard that is not addressed can lead to the misstatements of material that can be subject to regulatory scrutiny.

The following table provides an overview of important IFRS standards and gaps that are most typically found within institutions regulated by MAS:

| IFRS Standard | Key Requirement | Common Gap |

| IFRS 9 – Financial Instruments | Expected Credit Loss model | Backward-looking provisions only |

| IFRS 15 – Revenue Recognition | Performance obligation clarity | Bundled product mistreatment |

| IFRS 16 – Leases | Right-of-use asset recognition | Off-balance sheet leases |

| IFRS 7 – Disclosures | Market & liquidity risk disclosure | Insufficient narrative reporting |

Table 2: IFRS Standards and Common Reporting Gaps in MAS-Regulated Institutions

Challenges in the Gap Analysis Process — Lessons from Real Engagements

Practically, it is hardly ever easy to conduct a compliance gap analysis of an MAS-regulated institution. Organizational fragmentation is one of the most perennial issues; the case where compliance knowledge is isolated within the various departments that lack effective communication. This problem was experienced by a regional-based bank in the Middle East that had set up a subsidiary in Singapore when preparing a gap analysis before a renewal of the MAS license. The AML controls in the institution were upheld in its home jurisdiction by the group compliance team, which operated under a hybrid model that was never fully documented. The gap analysis showed that the local entity lacked an independent AML framework that would be able to meet the requirements of MAS on Singapore-specific customer due diligence, a critical finding that took months of remediation.

A disparity between the design of policy and its actual implementation is another typical issue. A European asset management firm, which had recently received a Singapore capital markets services license, found in a self-assessment two years into its operation that, on paper, and with respect to its formal guidelines of investment mandate, the firm was formally compliant with the requirements of MAS under the relevant MAS Notice. The outcome was a set of investment recommendations that technically violated the Notice, although there had been no intentional misconduct. This case demonstrates that a regulatory gap analysis should not only be based on document review – the human and operational layer is also a crucial factor.

Another area in which gaps are often found is technology risk. MAS Notice TRM (Technology Risk Management) places certain conditions on the system resiliency, penetration testing, and incident reporting. A payment services company that has been in the first MAS Technology Risk Management gap review found that although its cloud infrastructure has met the technical requirements of the Notice, it has never conducted an official tabletop exercise and has never documented a recovery time objective that would meet MAS thresholds. The remediation was to be done not just in terms of IT configuration but also in terms of the creation of new governance documentation and the appointment of a named technology risk officer – in other words, how a single gap area can have multi-dimensional remediation requirements.

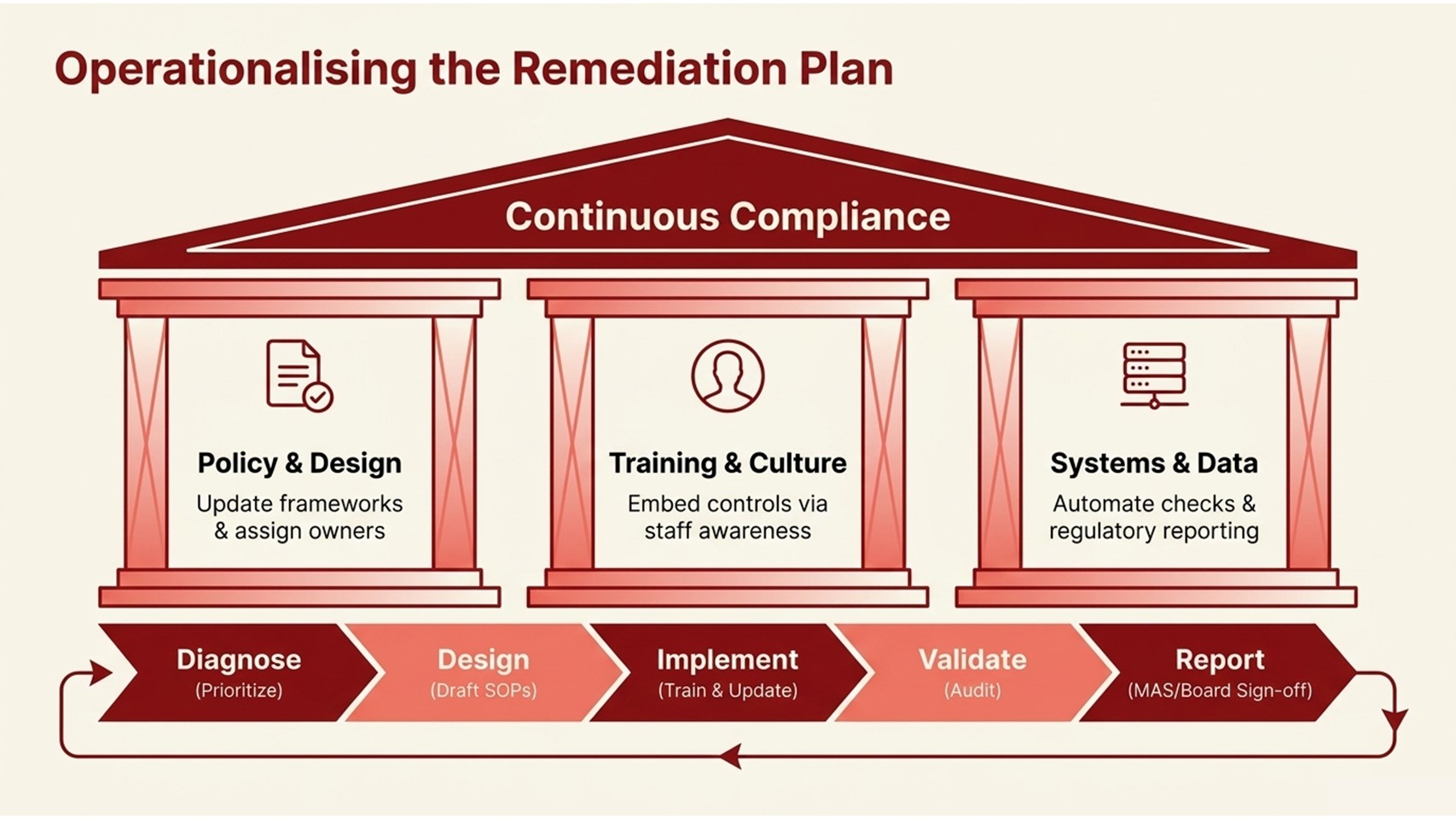

Operationalizing the Remediation Plan

The process of identification of gaps is just the start. The actual measure of the maturity of a compliance function is how well it is able to transform a gap register into sustainable operational improvements. The biggest mistake that many institutions make is to treat the remediation plan as a project with a specified end date – completing the necessary actions, closing the register and reverting to business as usual. The approach lacks the structural aim of the exercise, which is to establish a compliance culture and infrastructure that constantly complies with the MAS licensing compliance requirements instead of regularly catching up to them.

Remediation efforts need to be effective, and in this regard, three streams are intertwined. The former is policy and procedure redesign – ensuring that all written controls are revised to reflect current requirements in the MAS, are assigned to owners, and are subject to periodic review. The second is training and awareness – integration of the revised controls in the day-to-day conduct of personnel by way of a specific training program, escalation processes, and management reporting. The third is system and data infrastructure – making sure that the technology platforms in use in the institution support automated compliance checks, proper regulatory reporting and timely detection of incidents.

The remediation phase in junior and mid-level professionals can frequently be the place where the most concrete learning takes place. It includes direct contact with business units, technology teams and senior management and provides exposure to the full spectrum of the operations of an institution. Engaging in remediation workstreams even in a supporting role is a highly sought-after experience in compliance, risk, and regulatory affairs career paths. The following process flow describes a formal workflow of remediation followed by compliance teams throughout the region:

| Phase | Activity | Owner | Outcome |

| Diagnose | Examine the results of the gap analysis report. | Chief Compliance Officer | Prioritized gap register |

| Design | Prepared revised policies and control systems. | Compliance + Legal Teams | Rewrote SOPs and control documentation. |

| Implement | Training and system update roll-out. | HR, IT, Business Units | Employee skill enthusiasm, system harmonization. |

| Validate | Self-assessment and testing by internal auditors. | Internal Audit | Indication of the controls functioning well. |

| Report | Provide updates to MAS where necessary. | CCO / Board | Board sign-off / Regulator notification. |

Process Flow 2: MAS Compliance Remediation Workflow — Phase-by-Phase Execution

Conclusion — Actionable Insights for Compliance Professionals

One of the most useful exercises that a financial institution can conduct is a well-implemented MAS compliance readiness gap analysis, not only because it helps to manage regulatory risk but also because it is a step towards organizational improvement. The process makes institutions take a look at themselves, who know where their operations are not up to standard, and build the infrastructure to close those gaps in a structured, evidenced, and sustainable manner.

Among the insights that can be put into practice, some actionable insights are notable in the case of professionals in the junior-mid level stage of their careers. To begin with, take time to comprehend the particular MAS notices and Acts that pertain to the type of license that your institution has. Fluency in the regulatory framework is a core skill that differentiates those compliance professionals who are able to navigate the regulatory framework fluently from those who cannot. Second, treat the IFRS financial reporting transparency not as a purely technical accounting issue but as a facet of regulatory credibility. MAS anticipates that financial statements and regulatory returns accurately reflect the risk profile of the institution, and shortcomings in this area will draw the serious attention of supervisors.

Third, consider all gap analysis as a chance to create internal relations. Most successful compliance professionals are those who can collaborate with the finance, technology, operations, and legal teams to develop compliant and commercially workable solutions. Fourth, record all the evidence trail, as it is equally important as the remediation itself, since the MAS examiners will be seeking evidence that the controls work over time, and not just at the time of a gap analysis. Lastly, realize that regulatory gap analysis Singapore-based practitioners need to remain constantly aware of regulatory changes. Consultation papers, inspection findings and guidance letters are regularly published by MAS, and when each of these publications is made, it is an occasion to review the compliance posture of your institution before your institution is formally examined and then obligated to do so.

The institutions that are regularly performing well under the scrutiny of MAS are not the one that scrambles to prepare themselves for inspections but the ones that have entrenched the MAS licensing compliance requirements into their governance structure, their corporate culture, and into their day-to-day operations. A step towards that standard is a high-quality, truthful, and well-designed compliance readiness gap analysis.