Case Study: Standard Payment Institution License Advisory Supporting Regulated Payment Services in Singapore

Background on Case Study Standard Payment Institution License

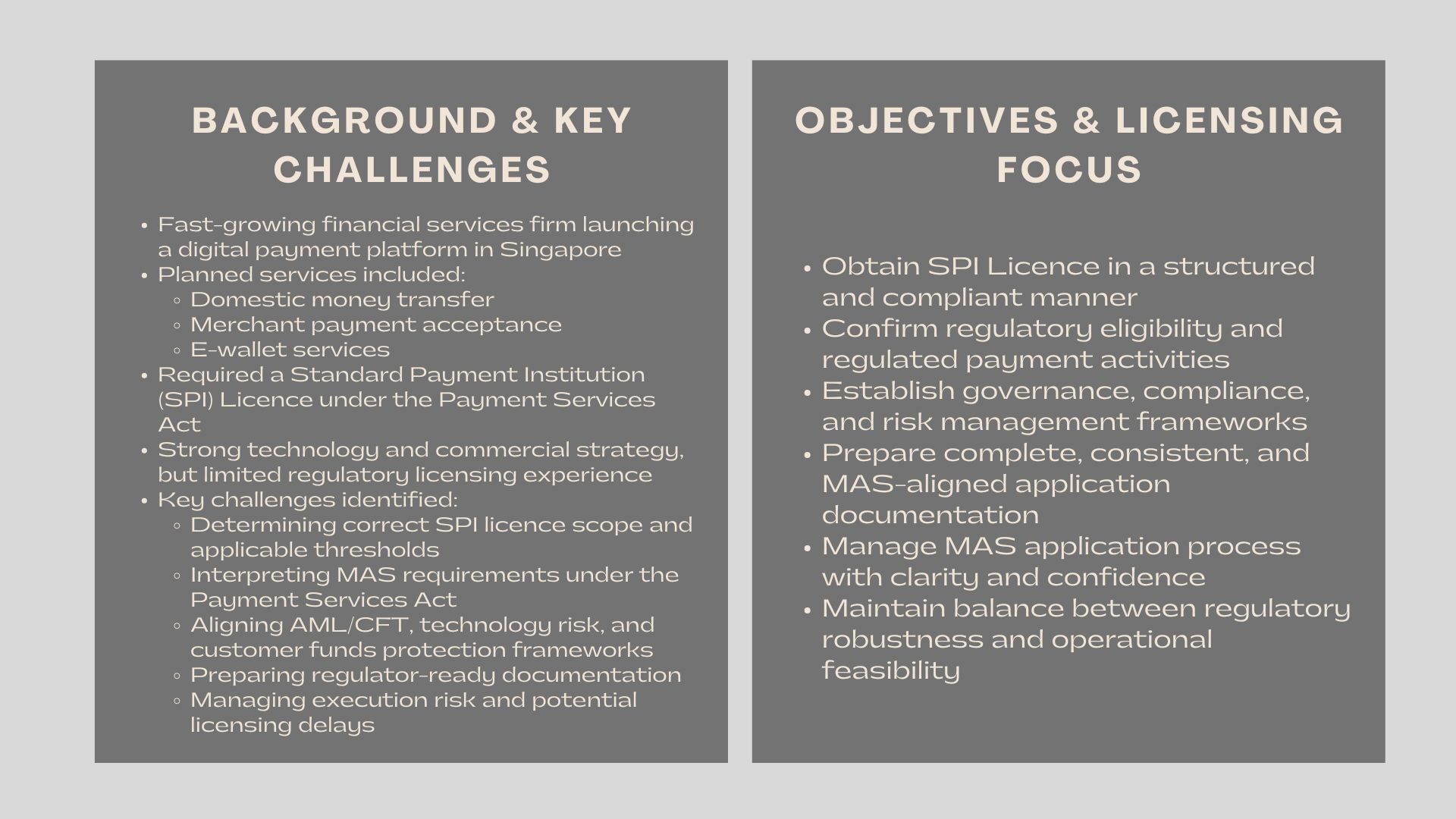

One of the fast-expanding an advance financial services firms was about to roll out a digital payment platform in Singapore and it would be offering domestic money transfer services, merchant payment reception services and e-wallet service. The company considered it necessary to conduct its operations under a Standard Payment Institution (SPI) Licence to be controlled by the Monetary Authority of Singapore (MAS) under the Payment Services Act as part of its market entry and compliance strategy.

Although the company possessed solid technology and a well-defined commercial roadmap, the management realised that to conduct regulated payment businesses in Singapore, it must have an effective licensing framework, good governance, and effective compliance strategies. The company involved itself in the service of professional advisory to guide through the process of application of the SPI licence effectively without compromising with the regulatory expectations of MAS.

In order to meet these needs, the firm has employed our Standard Payment Institution Licence Advisory Services to offer a complete solution to these needs with guidance being offered by regulatory assessment all the way to submitting the licence.

Issues and Challenges

The licensing process by the SPI has raised a number of regulatory and operational challenges that are usually encountered by payment services providers when venturing into the Singapore market.

The difficulty in deciding the right licence scope was one of them. The company required an understanding of what payment services were subject to the SPI regime, the application of transaction thresholds, and whether the activities that the company projected were within the limits of Standard Payment Institution.

The other difficulty was the interpretation of regulations. The Payment Services Act presents certain requirements that are associated with anti-money laundering and countering the financing of terrorism (AML/CFT), customer funds protection, technology risk management, and operational resilience. The company needed to be directed on how these requirements were practiced in the business model.

The documentation readiness was also a matter of concern. MAS requires the applicants to provide in-depth and consistent documentation of governance structures, compliance frameworks, internal controls, and business continuity planning. The current internal policies were to be refined to fit in the regulatory standards of the firm.

Also, the company was exposed to execution risk. The poor preparation or gaps in the licence application may lead to regulatory enquiries or delays which may have an impact on product launch schedules as well as commercial engagements.

Objectives

The main aim of the engagement was to guide the firm towards taking a Standard Payment Institution Licence in Singapore in a manner that was organized, compliant and timely.

In particular, the company aimed at:

- Existence of regulatory eligibility in the framework of SPI.

- Fully establish the area of regulated payment services.

- Instead, institute governance, compliance and risk management frameworks based on the expectation of MAS.

- Complete licence application documentation.

- Trade with confidence and regulatory transparency on the MAS application.

The engagement was meant to have a trade-off between regulatory strength and operational feasibility with both compliance and minimal administrative intent.

How We Helped

The advisory approach we used was based on a framework of structures and regulator-adherent approach in accordance with the Payments Services Act and MAS licensing requirements.

Our initial step included a regulatory scoping and eligibility test. This included scrutinizing the payment services that were proposed by the firm, the transaction flows and revenue model with the Standard Payment Institution regime and relevant transaction threshold.

Based on this evaluation, we have formulated a comprehensive SPI licensing road map that identifies the major regulatory requirements, documents deliverables and the expected schedules. This gave the management a clear cut and workable picture of the licensing process.

We assisted the company to create and institutionalise governance and compliance frameworks. This encompassed advisory of board and management duties, compliance supervision, internal controls as well as escalation procedures fit a licensed payment institution.

One of the major areas of the engagement was the formulation and fine-tuning of the necessary policies and procedures. These were AML/CFT Frameworks, Customer Due Diligence practices, transaction monitoring controls, protection of customer monies, and technology risk management practices. All the documentation was adjusted in accordance with the current operating model within the firm but to the requirements of the MAS.

We also helped in business continuity and operational resilience planning, which meant that the contingency measures, system controls and incident response procedures were properly recorded.

We also assisted in the preparation of the SPI application forms and other material as part of the licence application process. They were also focused on being clear, consistent, and complete so that friction with the regulations could be minimized and the review process could be smooth.

During the engagement, we collaborated with the management to change regulatory requirements into viable operational activities. This helped the company to create internal regulatory consciousness and compliance ownership at the very beginning.

Value Delivered

The case study is an example of how a regulated payment service provider can be facilitated by the use of structured Standard Payment Institution License Advisory Services into the regulated financial environment of Singapore.

The engagement assisted the firm in enhancing governance, demystifying regulatory requirements, and developing a compliance-appropriate operating platform through a regulator-consistent and practical advisory practice. The licensing preparations effort as well improved internal awareness of continuous regulatory obligations in the Payment Services Act.

The SPI advisory framework that was formed as a result of this engagement offered a powerful baseline of sustainable and legal payment services operations in the changing digital payments environment in Singapore