Compliance Manual for Financial Firms

The financial services industry is highly controlled within one of the most controlled environments in the world. For companies that have to deal with multifaceted cross-border deals, initial listings, and connections with institutions, a properly organized compliance manual is the key to a successful operation. Compliance is no longer a box-ticking activity – it is a strategic activity that ensures that firms do not face regulatory fines, loss of reputation and also the general loss of customer confidence.

The article is addressed to junior to mid-level professionals who work in financial firms, either in compliance, operations, finance, or client-facing roles. It is also applicable to the candidates who are about to enter the industry and who want to know the realities on the ground of how financial firms manage to maintain regulatory levels. The idea is to take you through the framework, operations, and issues that make compliance work, through examples and real-world observations and knowledge.

Anti-money laundering procedures, the strictness of valuation in financial due diligence, are but some of the most important areas that a compliance professional needs to master. It also looks at the intersection of corporate governance compliance practices with the daily operational decision-making. To the extent that you are onboarding a new client, reviewing a merger target or conducting an internal audit, the principles listed in this manual will be a good reference.

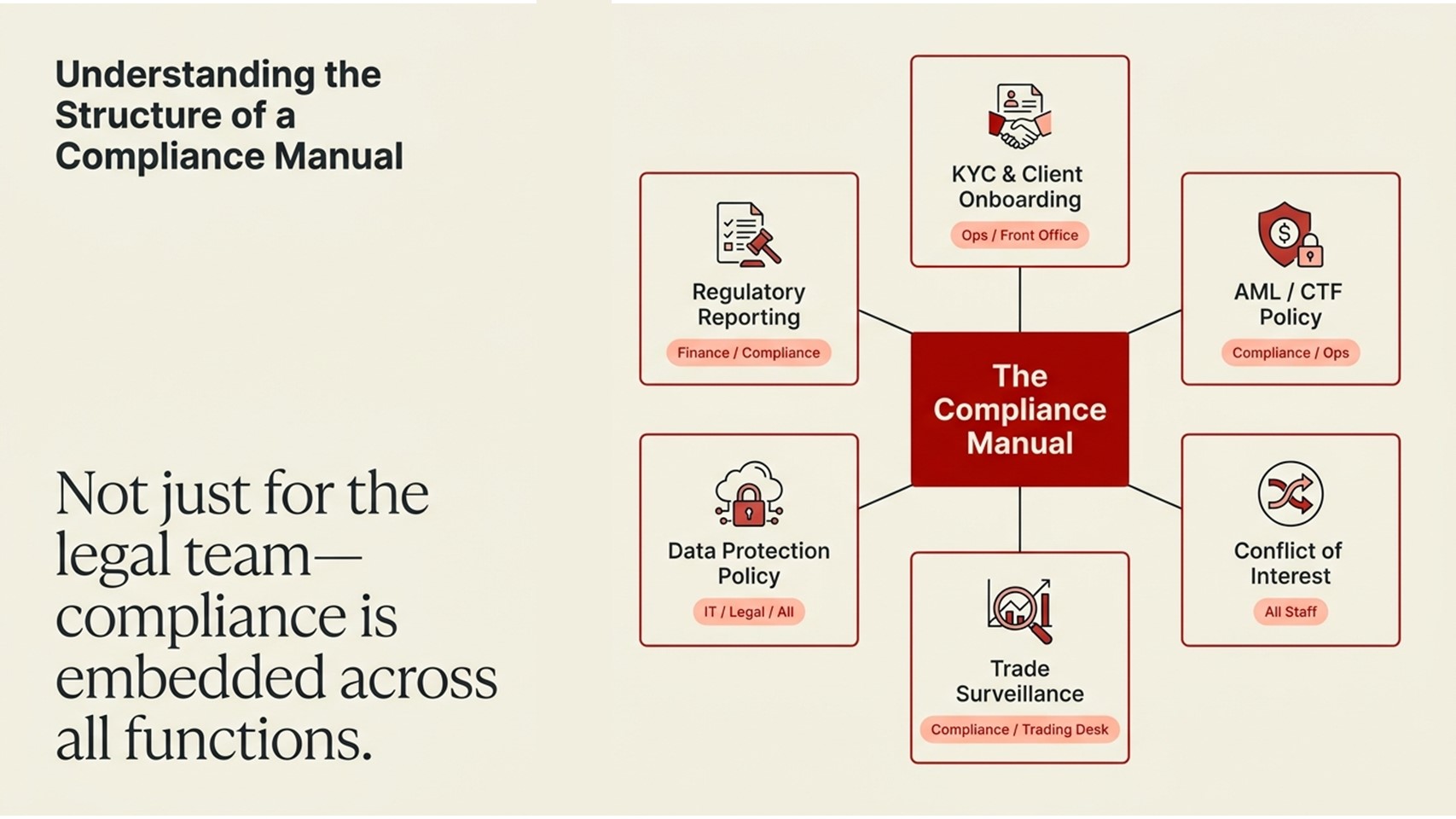

Understanding the Structure of a Compliance Manual

A compliance manual is a formal and living document that outlines how a financial firm complies with its regulatory requirements. It is a dynamic document, unlike a fixed policy document that is usually not updated with any changes in the law, regulation and best practice. To financial firms that operate under the jurisdiction of the Monetary Authority (in jurisdictions such as Singapore), the Financial Conduct Authority (UK) or the Securities and Exchange Commission (US), the compliance manual should reflect jurisdiction-specific requirements whilst maintaining globally consistent requirements.

Fundamentally, a properly organized compliance guide and Singapore-aligned framework usually encompasses the following areas: regulatory requirements and licensing conditions, client onboarding and Know Your Customer (KYC) procedures, anti-money laundering (AML) and counter-terrorism financing (CTF) policies, conflict of interest management, trade surveillance and market conduct, data protection and cybersecurity, and an escalation and whistleblowing policy. All these areas must be put down on paper with adequate details so that once a new employee joins, he/she can read the manual and know not only what but also why each requirement is necessary.

The first mistake that the junior professionals commit is that the compliance manual is a document that has to be read by the legal team only. The reality is that in their day-to-day operations, front-office employees, operations groups, and even finance controllers often face compliance touchpoints in their work. Knowing the makeup of the manual will enable the employees in all the functions to know when the situation needs to be escalated or even looked into. Companies that incorporate a sense of compliance into the greater corporate culture always outperform those companies that are simply guided by their dedicated compliance department.

Table 1: Core Components of a Financial Firm Compliance Manual

| Component | Purpose | Who Uses It |

| KYC & Client Onboarding | Authenticate client and evaluate risk. | Operations, Front Office |

| AML / CTF Policy | Identify and thwart financial crime. | Compliance, Operations |

| Policy of Conflict of Interest. | Address and report possible conflicts. | All Staff |

| Trade Surveillance | Check trading to detect misbehaviour. | Compliance, Trading Desk |

| Data Protection Policy | Protect the data of clients and firms. | All Staff, IT, Legal. |

| Whistleblowing Procedure | Allow anonymous reporting of violations. | All Staff |

| Regulatory Reporting | File the necessary papers with the regulators. | Finance, Compliance |

Valuation in Financial Due Diligence: Why Accuracy Matters

The need to conduct mergers, acquisitions, and investment transactions is one of the areas of compliance work that is highly technical in nature. Financial due diligence Valuation Valuation in financial due diligence describes the process of independent valuation of the worth of a target company or asset prior to a deal being executed. It has both direct compliance ramifications, with overstated valuations potentially facilitating fraudulent transactions, and understated valuations potentially disadvantaging investors or breaching fiduciary duties.

A prominent case out of Singapore is that of the German payment processing company, Wirecard AG. Before its collapse in 2020, the billions of euros of fictitious cash balances could go undetected over the years, due to the failure of due diligence. This case serves as a stark reminder that robust valuation in financial due diligence is not merely about applying the right financial model; it is about verifying the existence, ownership, and liquidity of assets through independent means.

The lessons learned by compliance teams are that due diligence checklists must be more than merely a review of financial statements. It should involve checking of key contracts, reviewing related-party transactions, checking regulatory correspondence, and stress-testing management assumptions. Where forecasts are used to value, the forecasts should be compared with the industry averages and tested to the utmost level of rigor. The compliance function need not possess the valuation model, although it should be empowered to pose the hard questions that the financial advisor/ investment team may not ask under the pressure of a deal.

Table 2: Common Valuation Methods and Their Compliance Risk Indicators

| Valuation Method | Typical Use Case | Key Compliance Risk |

| Discounted cash flow (DCF). | Valuation of a company (or project) privately. | Excessive optimistic estimates of revenues. |

| Comparable Company Analysis | Listed company benchmarking | Cherry-picking peer group |

| Precedent Transaction Analysis | M&A deal pricing | Utilizing old or non-comparable deals. |

| Net Asset Value (NAV) | Value of real estate or fund. | Risk of ownership and existence of assets. |

| Earnings Multiple (EV/EBITDA) | General corporate transactions | Normalisation adjustments manipulation |

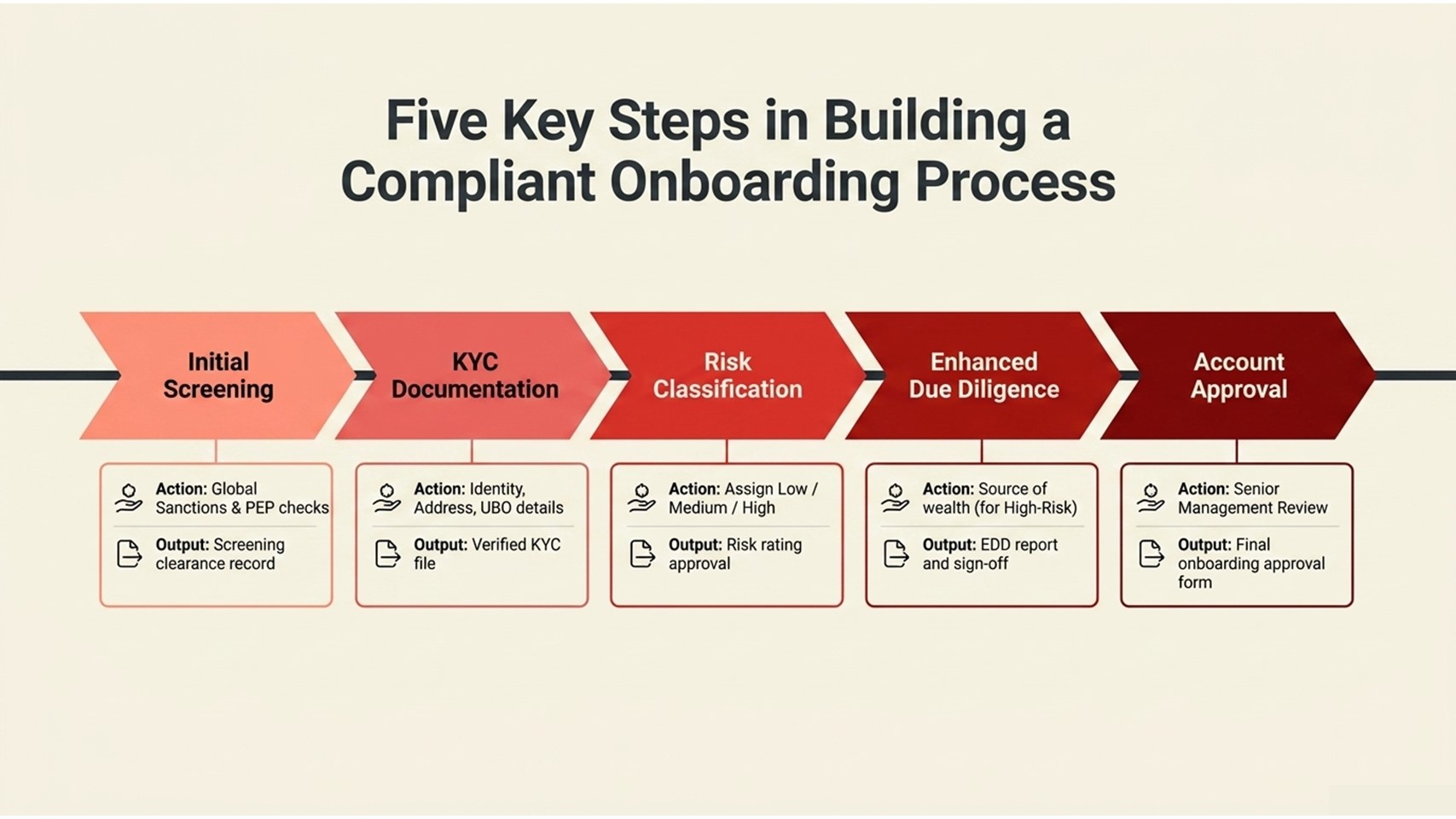

Five Key Steps in Building a Compliant Onboarding Process

The initial and, perhaps, the most important compliance touchpoint in the lifecycle of a relationship between a financial company is client onboarding. When it is done right, the entire engagement is set in a certain tone. The five steps outlined below reflect best practice in terms of onboarding in regulated financial markets, which are based on frameworks that have been used by international banks, asset managers and broker-dealer firms.

Process Flow 1: Client Onboarding Compliance Steps

| Step | Action Required | Responsible Party | Key Output |

| 1. Initial Screening | Screen name with sanctions and PEP lists. | Compliance / Operations | Screening clearance record |

| 2. KYC Documentation | Gather identity documents, address and UBO information. | Relationship Manager | Verified KYC file |

| 3. Risk Classification | Determine client risk score (Low / Medium / High) | Compliance Officer | Risk rating approval |

| 4. Enhanced Due Diligence | With high-risk clients, verification of the source of wealth. | Senior Compliance / Legal | EDD report and sign-off |

| 5. Account Approval | Last compliance and administration approval. | Compliance Head / CEO | Onboarding approval form |

The first step, initial screening, is a screening process run on the name of the potential client, aiming to identify any global sanctions imposed on the individual or organization in question, including but not limited to the following: the name of the prospective client; the name of the organization or business being considered; and the name of the individual or company being considered. It is an uncompromising condition both under the international AML principles and in the local financial legislation. This is now automated by widely-used screening software, but when potential matches are found, a process known as “hit review” is necessary.

The second and third steps of the onboarding process, namely KYC documentation and risk classification, are usually the points where the bottleneck occurs in the onboarding process. Clients will not be willing to disclose Ultimate Beneficial Ownership (UBO) information, especially when dealing with complicated corporate setups. The compliance professionals should be trained to communicate the regulatory grounds over such requests in a friendly and professional manner, and finally escalate to the senior management in case the client is not cooperating. The output of step three risk classification will indicate the need or otherwise of Enhanced Due Diligence (EDD) requirement in step four.

The fourth step, Enhanced Due Diligence, is applied to Politically Exposed Persons (PEPs) and clients in high-risk jurisdictions, as well as transactions of a certain amount of monetary value. This includes checking the source of wealth and source of funds by documentary evidence and verifying that the money came from a lawful and legitimate source and that the funds are lawfully and legitimately obtained. Final account approval should never be done without the involvement of a senior compliance signatory in order to ensure accountability and provide an audit trail. Companies that either omit or bypass these processes risk incurring huge regulatory fines.

Corporate Governance Compliance Practices: From Policy to Practice

Proper compliance practices of corporate governance are the gap between what the regulation and what the actual behaviour of the firm is. Governance frameworks define who is accountable to make decisions, how conflicts of interest are addressed and how accountability is ensured throughout the organisation. It is especially significant in the case of financial companies as they have fiduciary duties towards their clients, investors and counterparties.

Take the example of a mid-size European fund manager, who received a regulatory review in the early 2020s. The regulator discovered that although the firm had written policies regarding conflicts of interest and dealings between parties, these policies were not being systematically implemented. Board decisions regarding investment with related parties were passed without the records of the board meetings and the information to investors was not fully disclosed. The result was an official warning and the need to have an independent compliance monitor within two years. This case highlights one of the primary issues: it is not the same to have good policies on paper as to have good governance in action.

This is because most of the failures in governance happen in the gap between policy and practice, and a problem that is disproportionately experienced in smaller and mid-sized firms, where resources to comply are limited. In order to close this gap, companies ought to make investments in three aspects. First, governance education of all board members and senior management should not just be a one-time onboarding process, but a continuous provision of education on regulatory changes. Second, frequent independent internal audits, which seek to check the corporate governance compliance practices and documents being practiced. Third, there should be clear channels of escalation whereby the junior staff are able to point out areas of concern without fear of retaliation. The psychological safety in a compliance culture is equally important as the formal structure that forms its context.

Challenges, Lessons Learned, and the Road Ahead

Working in financial firms, compliance professionals have to deal with a number of structural and operational obstacles, which are worth knowing prior to entering the profession. Resource limitations are the most prevalent issue- compliance teams are commonly understaffed in comparison to the regulatory demands that the business will encounter. This poses pressure to prioritise, and even the decisions of prioritising are risky. A compliance decision, albeit unintentionally, has been made by a junior compliance analyst who fails to escalate an anomalous transaction due to the length of the queue.

The second significant challenge is the rate at which regulations are changing. Globally, financial regulators have greatly expedited their rulemaking in line with the changes in technology, crypto-assets and cross-border financial flows. An example of a compliance manual for a Singapore-based firm, e.g., must keep track of updates by various bodies in different jurisdictions, should it have international clients. The maintenance of the compliance manual is also a compliance requirement – companies have been fined for running their business on outdated compliance policies. Best practice would be to have each part of the manual owned by a specific compliance officer and to have a set of mandatory annual reviews.

Process Flow 2: Annual Compliance Manual Review Cycle

| Quarter | Activity | Owner | Output |

| Q1 (Jan–Mar) | Scanning regulatory horizon – discover impending alterations in regulations. | Compliance Officer | Regulatory change log |

| Q2 (Apr–Jun) | Manual review against the regulatory changes of the section-by-section of the manual. | Section Owners | Draft amended sections |

| Q3 (Jul–Sep) | Manual compliance within the business units: internal audit. | Internal Audit | Audit findings report |

| Q4 (Oct–Dec) | Board approval of new manual; staff recertification. | Compliance Head / Board | Updated manual v.[year] |

A third issue, and one which is proving to be more and more of an issue, is the conflict between commercial pressure and compliance requirements. Deal teams might be urged to expedite the onboarding of clients or to evade the improved due diligence to close a deal. The relationship managers might be reluctant to raise the issues about high-value clients for fear of ruining the business relationship. It is also at this point that the tone used at the top becomes quite critical – firms whose leadership teams actively champion the practices of corporate governance compliance are much less likely to see these pressures override proper process.

The experiences of the significant compliance failures experienced in the last decade are uniform across jurisdictions and types of firms. To begin with, documentation is important: when it is not documented, it has not occurred. Second, it is all about independence: the structurally impaired functions that report directly to the commercial leadership are all about independence. Third, valuation in financial due diligence and other technical tests should be challengeable and subject to independent review as opposed to being signed off by the deal team. Fourth, employees at all levels must know about their own responsibility – compliance is not the responsibility of someone else.

Conclusion: Actionable Insights for Compliance Professionals

Financial services compliance is challenging, dynamic, and is becoming more strategic. To professionals in the field or entering it, the greatest investment that you can ever make is in knowledge, not only of the rules, but also of the rationale behind them. The regulators are not opponents – they are at their best friends in ensuring the integrity of financial markets.

These are five of the actionable insights that can be gleaned from this guide. To ensure that your firm has an up-to-date compliance manual, it must be assigned a clear ownership and have its compliance manuals reviewed on a regular basis. Use high valuation in financial due diligence standards that transcend financial modelling to prove independently underlying assets and assumptions. Integrate compliance practices of corporate governance not only in policy documents but also in the daily decision-making culture of your company. Record all the details – your paper trail is your insurance. And never permit commercial pressure to be a cause of not going through due process.

The area has a great career development potential for individuals seeking jobs within the compliance sector because companies around the world are venturing into enhancing their regulatory capacities. The basic skills required and discussed in this manual, such as client due diligence, governance, valuations, and regulatory reporting, are the fundamental skills that every compliance professional must be able to master. Establish these pillars at an early stage, remain active in terms of regulatory changes, and do not consider compliance a cost centre but as an element of competitive advantage. Compliant firms are trusted in all aspects by clients, regulators and counterparties – and trust, in financial services, is the most valuable asset of all.