- 01 Introduction

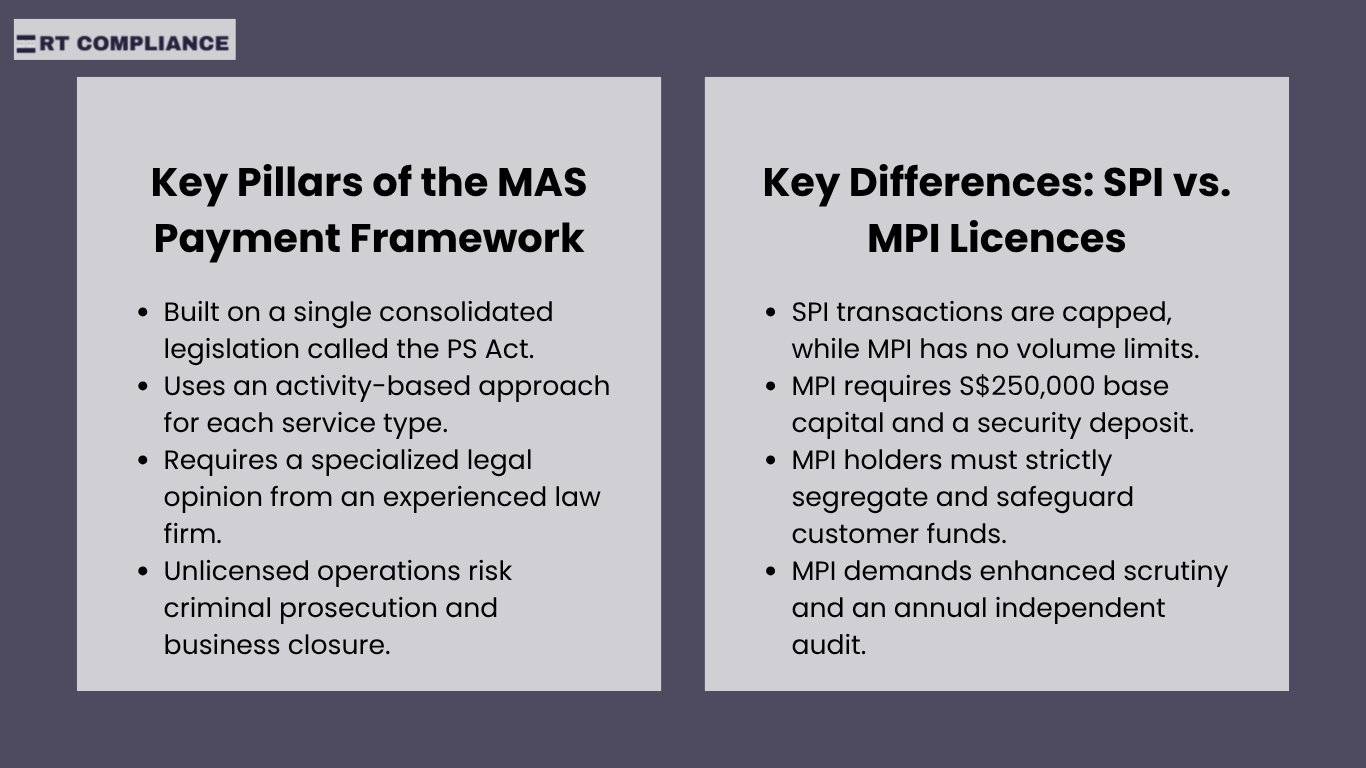

- 02 The Payment Services Act Framework

- 03What Is a Standard Payment Institution (SPI) Licence

- 04 What Is a Major Payment Institution (MPI) Licence

- 05 Key Differences Between SPI and MPI Licences

- 06 Payment Services Covered by MAS Licences

- 07Licensing Eligibility and Application Requirements

- 08AML/CFT and Compliance Obligations

- 09Common Challenges for Payment Institutions

- 10Choosing Between an SPI and an MPI Licence

- 11 Maintaining Compliance After Licensing

- 12Conclusion