What Are the Disclosure Requirements to Investors?

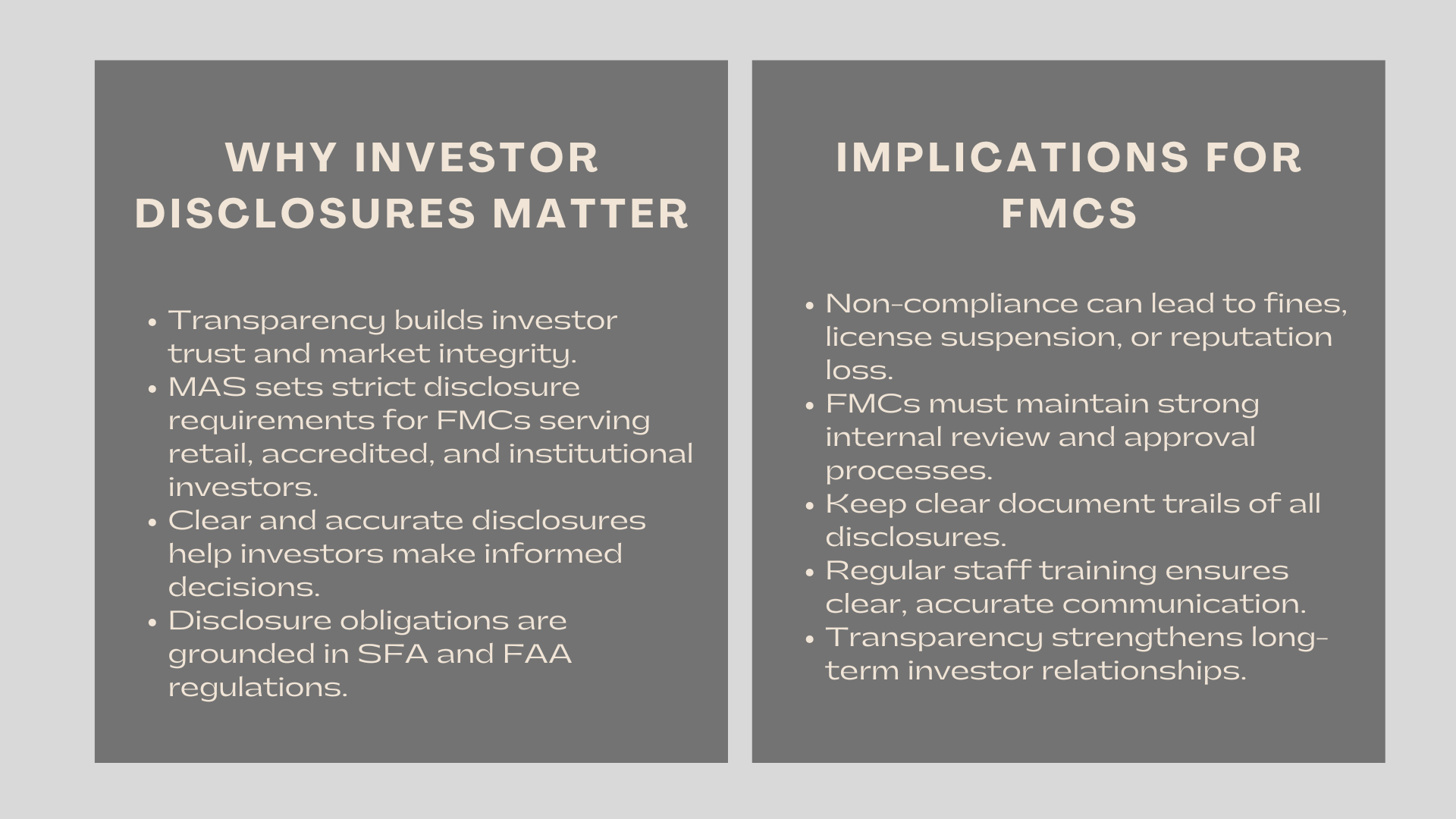

Transparency helps ensure both investors and the market remain protected in financial management. Investors are properly informed about their investments thanks to MAS investor disclosure requirements for fund management companies. MAS, as a regulatory body, has put in place detailed disclosure guidelines that fund management companies (FMCs) following should use when serving accredited, institutional, or retail investors.

Making sure investors receive proper disclosures allows them to decide wisely and trust the manager more. The article looks at the set of regulations, the different kinds of disclosures needed in each investment step, and how this impacts the overall activities of fund management companies in Singapore.

Regulatory Framework Governing Disclosures

Various instruments, including the Securities and Futures Act (SFA), Financial Advisers Act (FAA) and their respective regulations and guidelines, make sure disclosure obligations are enforced by the MAS in Singapore. FMCs are required to comply with these provisions no matter if they are licensed, registered, or exempted.

The main requirement of these regulations is called fair dealing, which means customers should not be misled or mistreated by the financial institutions. This means you should provide the right and complete details about the company when required.

What must be disclosed is different for each investor that the FMC deals with. Professional and institutional investors can be offered more individualised information, but retail investors are obliged to receive complete and easily accessible facts, as they usually have less understanding about financial matters.

Pre-Investment Disclosures: Setting Expectations

Before giving money, the FMC is bound by law to give full details about anything that could sway the investor’s decision. Normally, the pre-investment disclosure comes in the form of offering documents such as a prospectus, information memorandum, or private placement memorandum. These represent pre-investment disclosure obligations for retail and institutional investors, helping them make informed choices.

It should be explained in these documents how the fund will invest, what goals it aims for, and what kind of assets it includes, plus how those assets are managed. The disclosure should point out the possible risks connected to the investment, especially those related to the market, borrowing, liquidity, or concentration of the investment.

Another important topic is making fees and charges clear to people. Investors should know that management, performance, and all other workplace fees will be deducted from the money they invest. The information about these fees must be easy to spot and not described in the small print.

Once in scope, accounts can offer details about borrowing funds, working with derivatives, or using hedging strategies. All of these elements may determine affect how risky or valuable the fund is and so must be told in full.

Government standards request that limited partnership or unit trust funds give investors the needed documents, including identifying agreements or trust deeds.

Ongoing Disclosures: Keeping Investors Informed

As soon as someone becomes a fund investor, the fund manager must supply timely and correct information. Periodically, the fund has to share information about its performance, the level of its assets, and any observed risks. All of these are part of the ongoing reporting and transparency requirements for investors that MAS expects firms to follow.

Managers of funds should provide timely reports, whether they are monthly, quarterly, or annual, showing the portfolio structure, standing over similar indexes, NAV, and any major shifts in the investment plan. When these reports are made for retail investors, they should be simple to read and sometimes include illustrations or extra explanations.

Whenever there are important changes to the fund’s investment strategy, its manager, staff, or service providers, these changes must be stated promptly. The organization should ensure the change’s reason and any effect on investors are well explained.

Any event that makes a serious difference to the fund’s outcome or process, for example, overstepping investing limits or prohibiting investors from withdrawing, should be announced quickly. MAS hopes that firms will be clear and share regular information until the issue is settled in such cases.

Managers of funds for retailers need to frequently update their offering documents and notify MAS as well as all investors if any changes occur. It makes certain that accurate and relevant disclosures are provided all during the fund’s life.

Conflict of Interest and Fee Transparency

It is very important for investors to know when corporations have conflicts of interest. They must find times when their or their affiliates’ goals contrast with those of investors, if they do exist.

For instance, these may be transactions between a fund and its related entities, trading conducted by fund managers for themselves, or systems for paying bonuses that come with an incentive for the wrong kind of investment. When conflicts exist and they cannot be avoided, they are to be revealed in an open and detailed way.

It is not enough to mention conflicts due to “various factors” without giving details. To comply with MAS, companies should explain clearly and in detail the conflict of interest and how they address or overcome it.

The compensation received by the fund manager should also be well explained in similar disclosures. The fees come from base management, certain performance fees, and any deals with brokers or similar organizations using soft dollars.

Investors should be told the effect of fees on their earnings and asked if any special perks given to the manager could influence the investment policy.

Implications for Fund Management Companies

Refusing to follow disclosure standards may result in important legal and publicity problems. MAS regards situations where updates and details are either lacking or are mispresented as a violation of FMC conduct and may apply certain penalties, ranging from small fines to suspending the license or issuing public warnings.

In addition to rules, a lack of information for investors can bring about lawsuits or harm a company’s reputation if someone claims he or she wasn’t properly notified about the risks.

FMCs should put in place solid internal procedures for the creation, review, and distribution of all disclosures. It means that the legal, compliance, and risk teams must help with preparing and approving offering documents and investor messages.

All personnel responsible for work with clients and fund reporting need ongoing training every so often. Team members have to know the information that should be disclosed and also how to present it honestly, clearly, and without misleading others.

Additionally, it is important for FMCs to have a document trail of every disclosure made to investors. Such communications are emails, presentations to investors, and meeting minutes, which can be checked when a regulatory query arises.

Conclusion to What Are the Disclosure Requirements to Investors

Investor protection and following the rules fit together with requiring disclosures in the fund management industry of Singapore. No matter if they are serving institutions, accredited clients, or retail, these companies should approach clients with a clear and emphasize their needs when sharing information.

Maintaining MAS rules, being honest, and putting rules into place keep investors’ trust and maintain the fund managers’ relationship with them.

Since the financial industry is highly liberalized and strictly regulated, transparency goes beyond regulations and makes reputable firms ahead of the rest.